Origin Materials - A Carbon Negative Moonshot

Origin Materials - A Carbon Negative Moonshot

May net zero refer only to your carbon footprint

Note: For entertainment and informational purposes only. Not investment advice. Please do your own research.

This is how Origin Materials [site] describes itself:

Origin Materials is the world's leading carbon negative materials company.

Origin’s mission is to enable the world’s transition to sustainable materials.

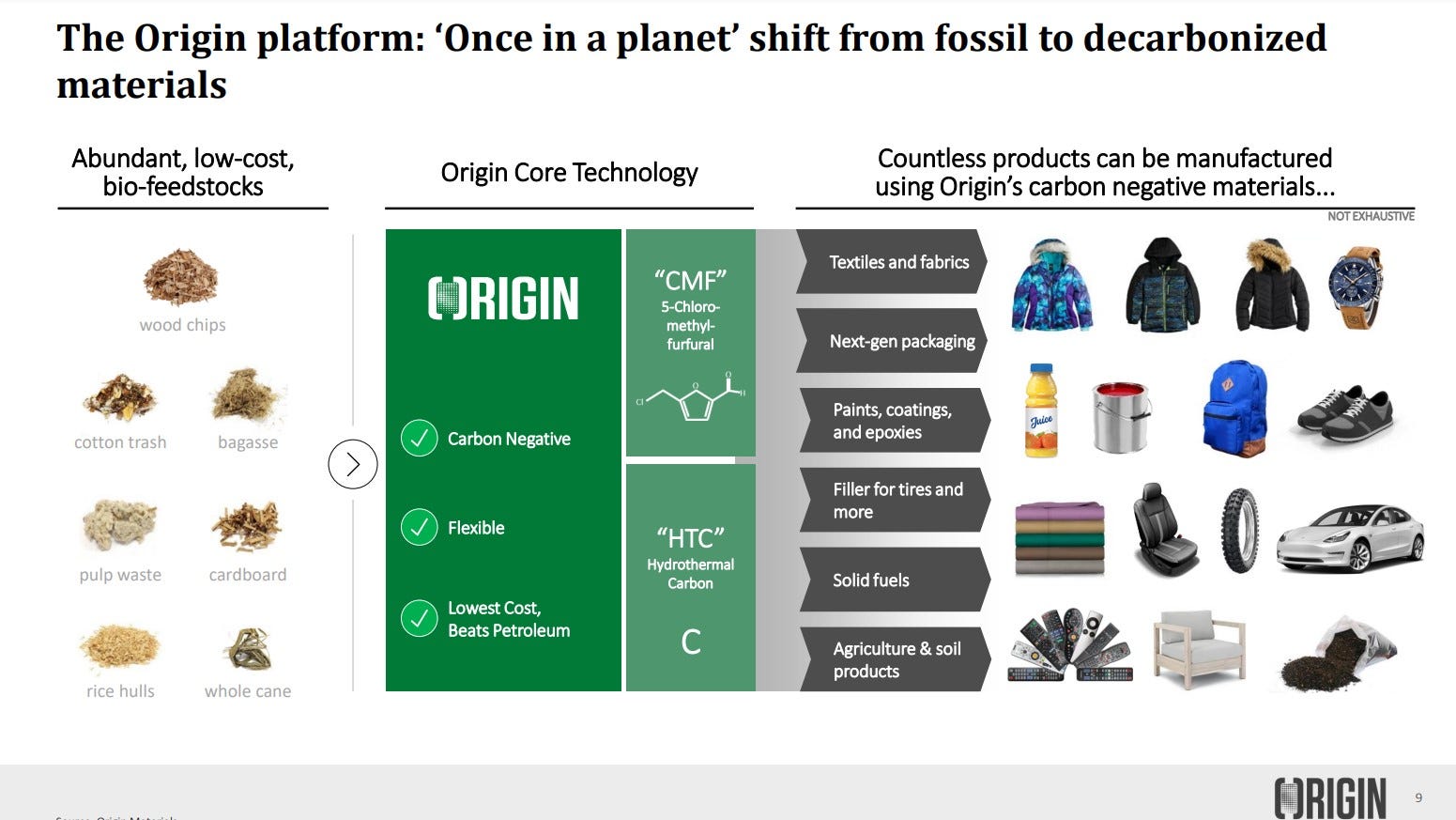

Over the past 10 years, Origin has developed a platform for turning the carbon found in inexpensive, plentiful, non-food biomass such as sustainable wood residues into useful materials while capturing carbon in the process.

Origin’s patented technology platform can help revolutionize the production of a wide range of end products, including clothing, textiles, plastics, packaging, car parts, tires, carpeting, toys, and more with a ~$1 trillion addressable market.

In addition, Origin’s technology platform is expected to provide stable pricing largely decoupled from the petroleum supply chain, which is exposed to more volatility than supply chains based on sustainable wood residues.

Origin’s patented drop-in core technology, economics and carbon impact are supported by a growing list of major global customers and investors.

In short, the company claims to have figured out how to turn wood residue into plastics and other useful materials in a process that is:

carbon negative;

cost-competitive with petroleum-based products; and

can be dropped into existing supply chains.

Earlier this month, the company announced that its core materials chloromethyl furfural (CMF) and hydrothermal carbon (HTC) are now able to display a unique USDA certified biobased product label [press release].

The company raised ~$470M cash via a SPAC in order to commercialize its technology and fund the construction of two plants. Since completing its SPAC merger with Artius Capital in June 2021, the stock has cratered, along with the rest of the SPAC market. It’s traded between ~$5-$7 over the past few days.

At these levels, this strikes me as a fascinating moonshot venture idea that happens to be publicly traded.

What is Origin?

The following Analyst Day presentation (April 2021) provides an excellent overview of the company.

The following are the three key investor presentations:

Origin Q2 presentation - August 2021 [link]

Analyst Day Presentation - April 2021 [link]

Investor Presentation - February 2021 [link]

Investment Highlights

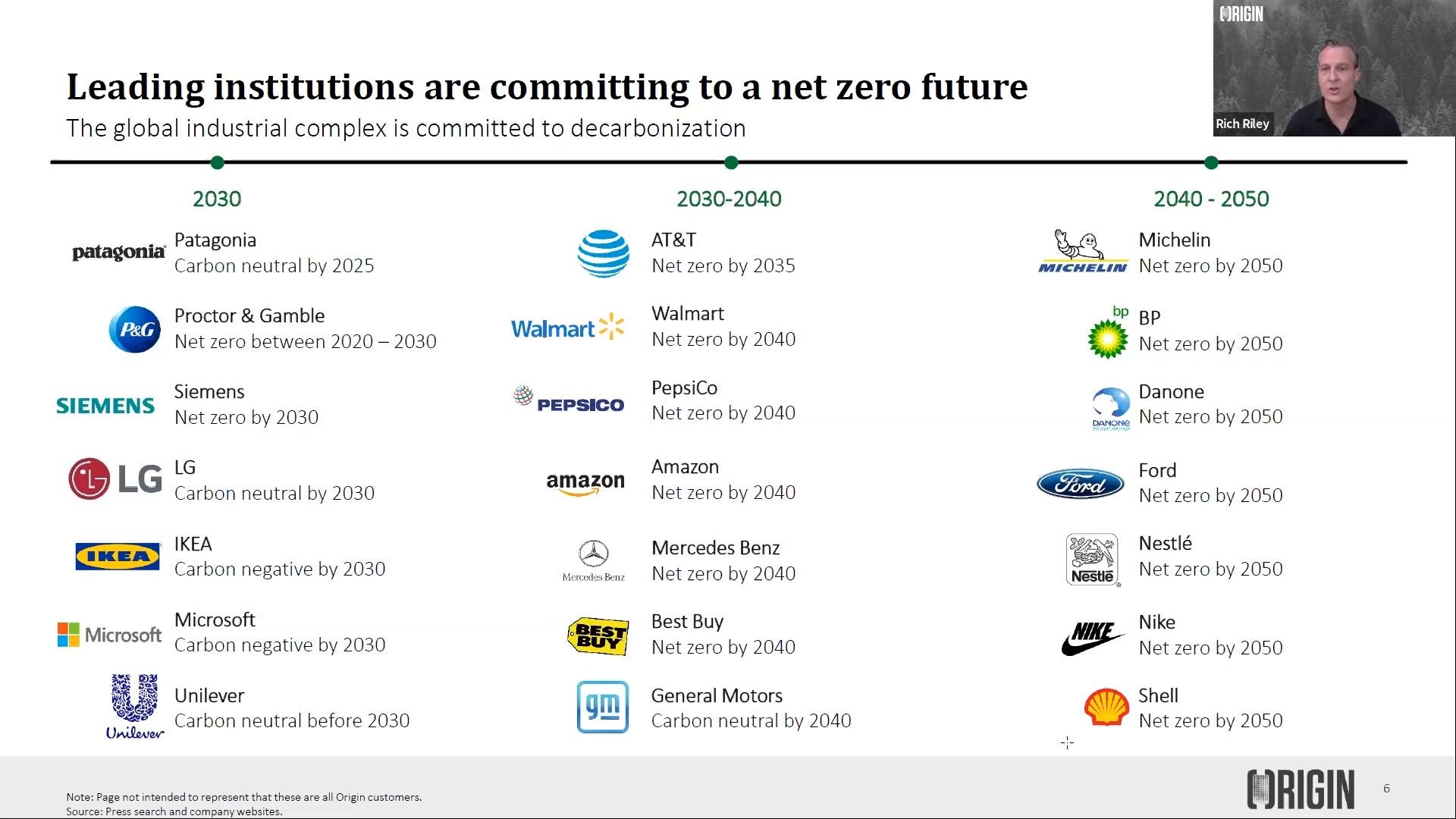

1. Governments and corporations are declaring aggressive decarbonization and net zero goals in the coming decades.

2. Origin has developed a technology that can make plastic (among many other materials) out of wood residue (sawdust, wood chips), rather than petroleum.

Origin claims its solution is superior as it is:

Drop-in ready, supply-chain ready, and therefore scalable and adoptable by the industry as a viable alternative to fossil-based feedstocks

Negative-to-low carbon as its feedstock can be sustainably harvested and renewable

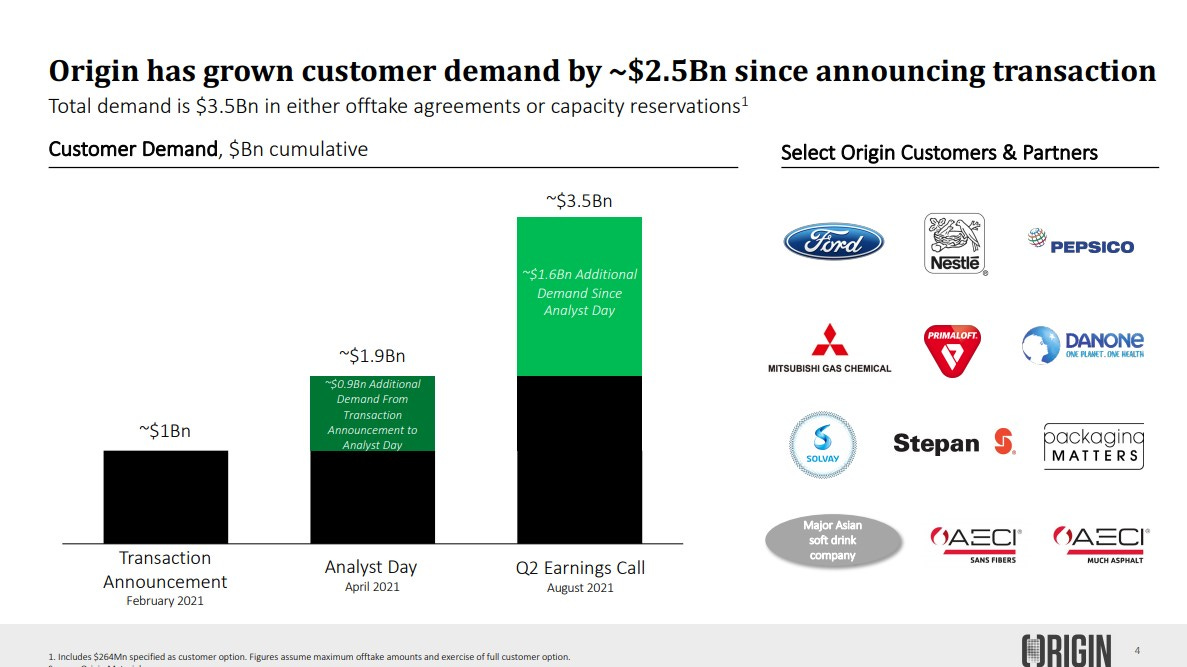

3. Origin’s technology has been vetted by leading consumer products companies such as PepsiCo, Danone and Nestle, among an increasing growing list. The company claims to have tripled capacity reservations since February and now has capacity reserved for $3.5B (August 2021).

Origin has claimed its technology will “revolutionize the production of a wide range of end products, including clothing, textiles, plastics, packaging, car parts, tires, carpeting, toys, and more with a ~$1 trillion addressable market.” In their Q2 earnings release, the company announced a number of commercial deals with leading companies representing these other verticals that indicate the broad applicability for this technology.

Examples include:

Automotive - Ford Motor Company and Solvay. Origin and Ford are launching the Net Zero Automotive program focused on industrializing new materials to drive decarbonization in the automotive industry, with potential applications through the interior and exterior of the vehicle, including bumpers, paint pigment, door panels, tire filler, underbonnet foam sheet, black plastic, head rests, seat cushions and arm rests.

Chemical - Mitsubishi Gas Chemical. Mitsubishi will utilize Origin technology to industrialize advanced carbon negative chemicals and materials for applications in the automotive, medical, food, information and communication, energy, and infrastructure sectors. Mitsubishi was also an investor in the PIPE.

Apparel - PrimaLoft. PrimaLoft will develop carbon negative insulating fiber for outdoor gear, bedding and apparel. PrimaLoft’s brand partners include Patagonia, Stone Island, L.L. Bean, Lululemon, adidas and Nike.

Packaging - Packaging Matters. To advance carbon negative packaging solutions, building on an existing 10-year supply agreement.

Supply Chain - Palantir Technologies. To accelerate the world’s transition to net zero carbon with a focus on decarbonizing the global materials supply chain.

During the Q2’21 earnings call [transcript], management provided additional color on the customer contracts:

So they're typically over $100 million. They're 5 to 10 years in length and they're typically with big companies and they would normally start with what we call a capacity reservation, which specifies the product, the price, the quantity and the duration of the contract. And then we'll move that into an offtake agreement, certainly in time for project financing of the plants.

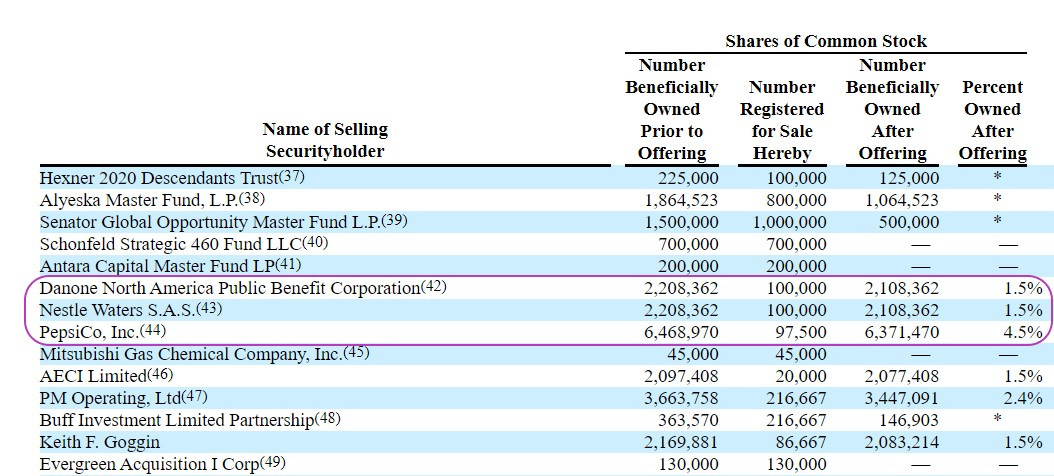

4. PepsiCo, Danone and Nestle have also invested ~$40M and own ~8% of the company [prospectus]. A partial cap table is shown below.

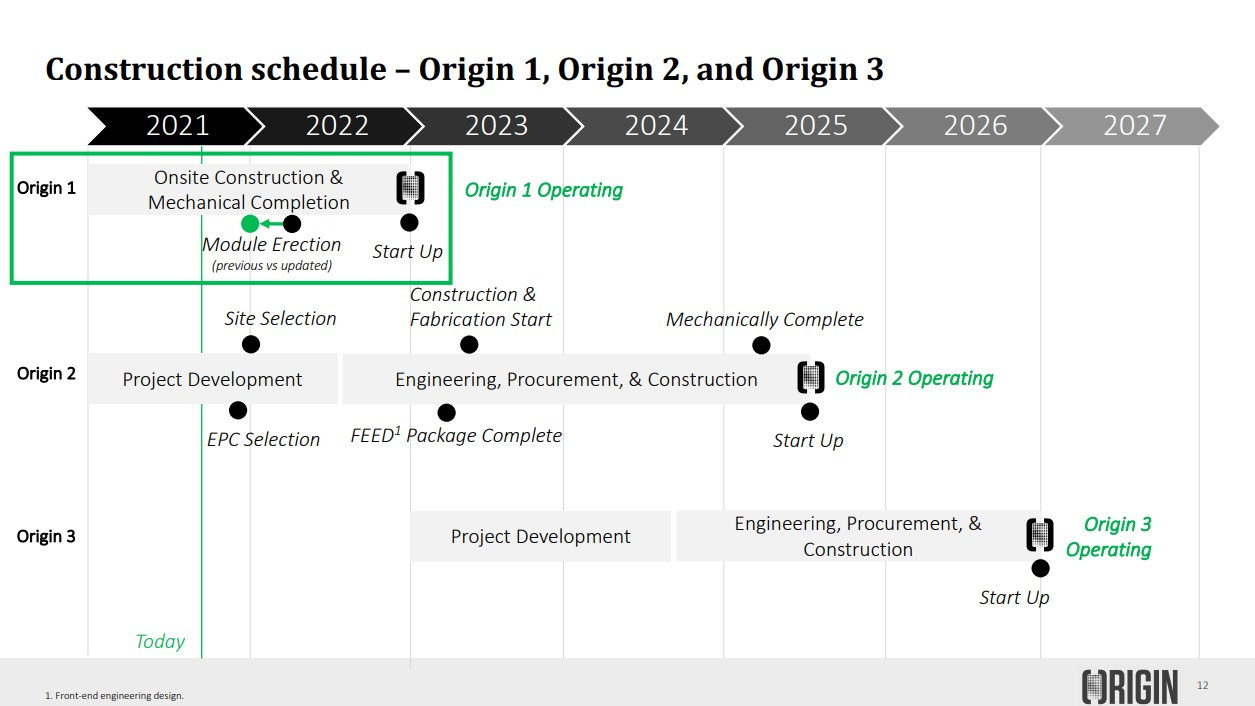

5. The company now needs to prove out commercial scale of their technology to produce these materials. They are building two plants - Origin 1 and Origin 2 - slated for delivery in late 2022 and mid 2025. Origin 1 is meant to be more of a proof-of-concept facility, while Origin 2 is meant for commercial scale.

As of Q2, they are tracking ahead of the schedule laid out during the SPAC process for Origin 1. Note that these facilities have been delayed many times before.

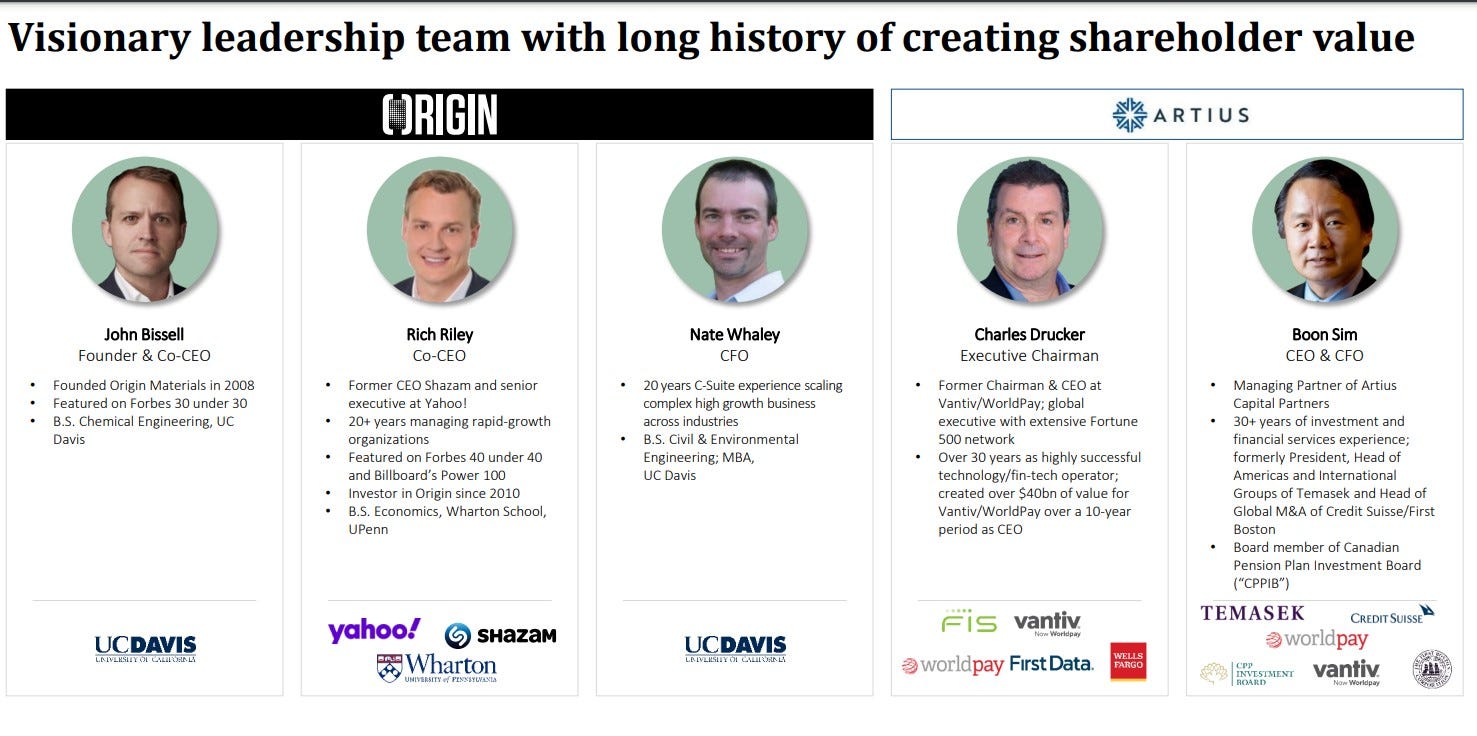

6. Artius, the SPAC sponsor, conducted extensive diligence and have excellent track records in the finance and corporate realm. Charles Drucker was former Chairman and CEO of Vantiv/WorldPay, and Boon Sim previously was Head of Global M&A at Credit Suisse and Head of Americas and International at Temasek.

In the intro to the Analyst Day video, Boon Sim noted that the team conducted over 3 months of extensive due diligence on Origin:

Retained Bain Consulting and two specialist chemical consulting firms to vet the technology, scalability, unit economics and total addressable market.

Conducted 40+ key customer and potential customer calls. Covered key customers like Pepsi, Danone and Nestle. All of these key customers confirmed to them that the technology works and extensively tested by them. Confirmed that it is the only company that produce carbon negative materials that has an ISO compliant Life Cycle Assessment (LCA) report from Deloitte [link] to support their claims.

The Artius team was very involved in the diligence [Prospectus]:

During the weeks of January 18, 2021 and January 25, 2021, representatives of Artius and its advisors held multiple teleconferences with Origin and its advisors to continue to conduct due diligence of Origin’s business. These conversations included (i) several due diligence calls with key customers, (ii) intellectual property due diligence discussions on January 21, 2021, January 26, 2021 and January 29, 2021, (iii) financial forecast and plant economics discussions on January 18, 2021, January 22, 2021, January 23, 2021 and January 25, 2021, (iv) technical due diligence discussions on chemistry technology and manufacturing processes on January 21, 2021, January 22, 2021, January 27, 2021 and January 28, 2021, (v) capital requirements, plant design and construction diligence discussions on January 25, 2021 and January 27, 2021, and (vi) a legal due diligence discussion on Jauary 27, 2021. Several of these teleconferences were attended by members of the Artius Board of Directors.

An investor posted lengthy notes on Twitter to two calls (July 2021, June 2021) with Origin’s management team and the SPAC sponsors.

40 customer calls, 60-90 minutes long, and Boon and Charles were on each one

Engaged two major consultants to assess the technology, patents and unit economics

Product is chemically identical to PET, which has been confirmed by Nestle, Danone, and Pepsi. Those customers alone could satisfy demand worth ~$8B and account for 20 manufacturing plants.

The sponsors are in it for 5-10+ years

The key to their thesis is that the product is cost competitive with petroleum-based products.

The board of directors also seems to offer extensive and relevant experience across chemicals (Du Pont, BP) and consumer products (Clorox, P&G). The CEO goes into detail on each board member’s strengths in the following Reddit AMA video.

How is Origin using its BOD from the chemical industry to grow the business?

Karen Richardson - BP and high growth - Chair role

Benno Dorer - CEO of Clorox - they are excellent at chemicals products and understand consumer

Kathy Fish - Chief Product Officer at P&G - using performant materials in consumer products

William Harvey - Du Pont, ran packaging arm - understanding from large scale producers of product

7. Construction and execution is the key risk, but the company appears to be taking the right steps to mitigate.

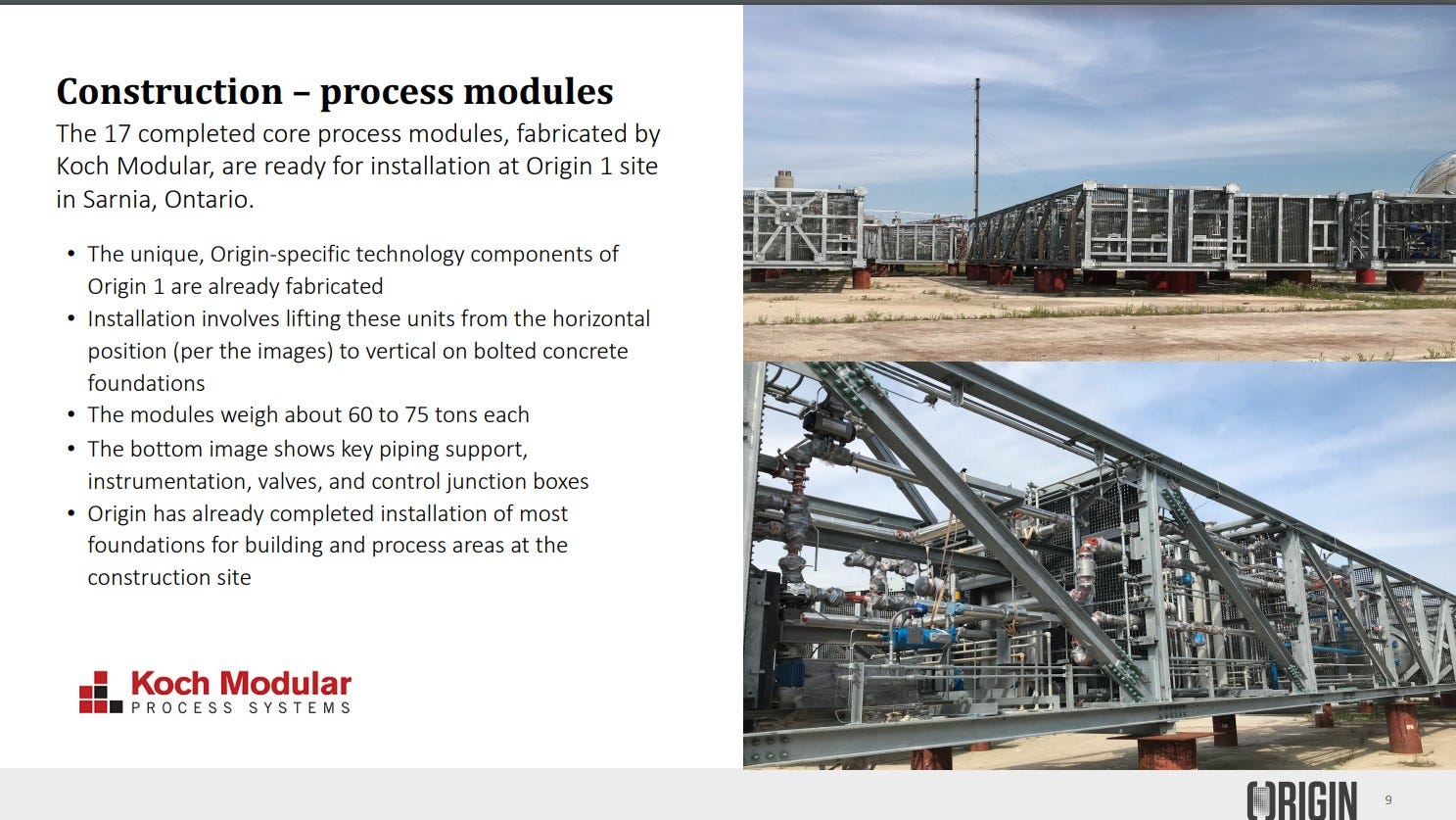

Koch Modular (Koch Industries subsidiary) is the construction partner for Origin 1.

From the earlier referenced management call notes, Koch had given performance guarantees on the hydraulics, thermal and mechanical performance of the construction of the plant.

In the Q2 earnings presentation, the company noted that the core modules were ready for installation.

The company also claimed to have sufficient capital to complete both plants with $100M to spare.

8. Insiders have demonstrated their bullishness by backstopping the deal.

The deal announcement in February 2021 was made at the height of the SPAC frenzy and included an oversubscribed PIPE.

Transaction is expected to provide up to $925 million in gross proceeds, comprised of Artius’ $725 million of cash held in trust, assuming no redemptions, and an oversubscribed $200 million fully committed PIPE at $10.00 per share, including investments from Danone, Nestlé, PepsiCo, Mitsubishi Gas Chemical and AECI, as well as certain funds and accounts managed by Sylebra Capital, Senator Investment Group, Electron Capital Partners, BNP Paribas AM Energy Transition Fund and affiliates of Apollo.

Legacy Origin customers and investors Pepsi, Nestlé and Danone purchased 97,500, 100,000 and 100,000 shares of our Common Stock in the PIPE transaction.

Since then, the SPAC markets have endured a tough past few months. Recently completed deals have had massive redemptions.

The Origin deal was also subject to a minimum $525M closing cash condition. This was put at risk as the company sustained a high level of redemptions.

In order to close, Apollo invested another $30M into the deal as part of a backstop agreement [June 14, 2021]. The SPAC sponsor Charles Drucker invested another $6.5M in the PIPE at the deal closing. [Form 4]

While the SPAC sponsor did get ~18M shares by getting the deal over the finish line, they had also agreed to a number of vesting restrictions for 4.5M of those shares subject to share price performance conditions.

As can be seen from the cap table and footnotes below, there are currently 136.7M shares outstanding, but there can potentially be up to ~210M shares assuming the stock reaches $25 per share.

After the deal closed, the stock subsequently collapsed to ~$5.

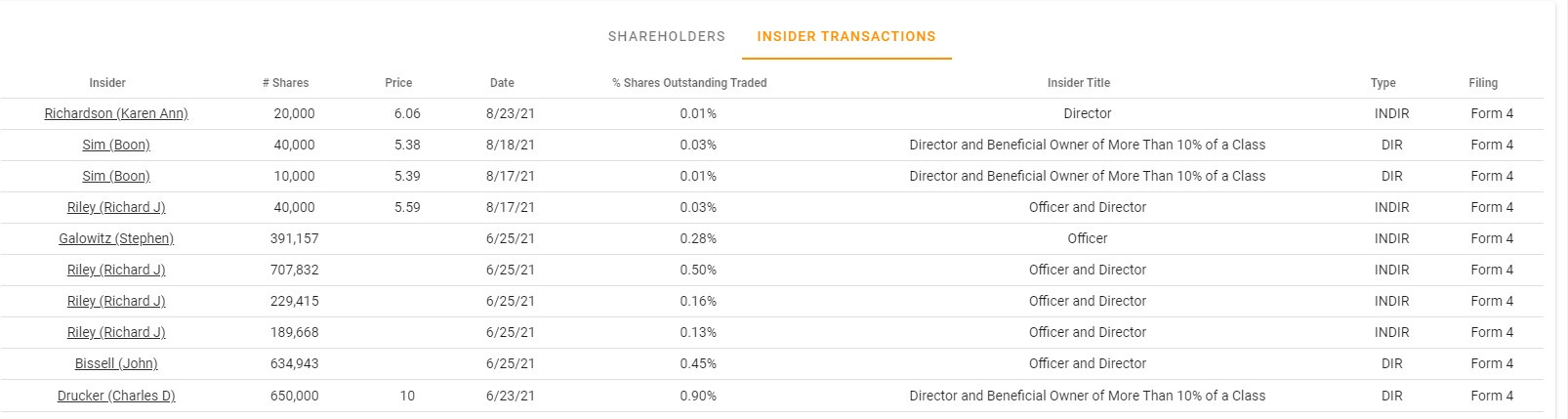

The board chair Karen Richardson [Form 4], SPAC sponsor Boon Sim [Form 4], and co-CEO Rich Riley [Form 4] have all made purchases in the past week.

While insiders may choose to sell for a number of reasons, when insiders exhibit cluster buying on the open market, that generally is a good indicator that the stock is undervalued.

Risks

Technology risk: Seems too good to be true. Is this Theranos, or is this not? As a pre-revenue company, there is a significant risk that this all goes to zero, even if the technology works out. It’s hard to dismiss the growing list of legitimate customers, many of whom are investors. Hopefully this is not a crowded trade relying on the diligence and conviction of others. I may very well be guilty of that myself.

Execution / Construction risk: The construction could be delayed, it turns out to be much more costly than originally estimated, etc. The company has already missed delivery deadlines in the past, though that seems to have been before Artius’ involvement. At the current price, the market seems to be expecting bad news, that it’s inevitable that this will get delayed. It doesn’t seem to give much credit to the company tripling its offtake volumes this year. It seems odd that there seems to be less skepticism on the technology, and more in the construction. Skepticism for SPAC companies is warranted. If the company is successful in proving out Origin 1, then I would expect the market to dramatically adjust their expectations accordingly.

Financing risk: Management claims they will still have $100M remaining even after completing Origin 2. They’ve also indicated that their financing assumptions (50% LTV to 70% LTV) may be conservative. I’m skeptical that their current cash balance is sufficient, but I feel confident that their investor base will help them bridge the gap. My hunch is that some of their existing investors (e.g., Apollo) may also be involved in future debt financings to fund their construction projects.

Commercialization risk: Even if the plants are eventually built, it may turn out that the technology cannot be deployed cost-effectively at scale. Many of the customer offtake agreements have exit clauses in the event certain deadlines are not hit. Management is confident that any such restrictions could be extended because their customers are looking for this solution. If it turns out Origin’s materials are not actually cost-competitive, then that may change their appetite to wait or to purchase in volume. However, management believes there are opportunities to pursue joint ventures with industry players to license the technology, so even if these plants do not work out, there may still be value in the technology regardless if the company is unable to commercialize the technology successfully themselves.

Competition risk: Is this truly a unique technology? I am not smart enough to say otherwise. The Deloitte LCA report was over my head. Management claims there is a significant process advantage given their multi-year headstart with this technology. Again, I recognize that I am relying on the diligence performed by Artius as well as the customer announcements. At this price, it’s not necessary for the the technology to be truly unique, as long as there customer demand for the end product.

Valuation

The stock has been extremely volatile over the past few weeks, and a 10% daily swing is to be expected.

With 136.7M shares outstanding and ~$470M net cash on the balance sheet, a share price of $5 to $7 implies the enterprise value is ~$200M to ~$500M.

Even with the cash balance, there is a meaningful risk of ruin here, but the upside is undeniable. Setting aside the investment component, there is also the giddy hope that a technology like this could actually work.

I’m opportunistically building an ~1% moonshot position and looking out for the following milestones:

Origin 1 modules installed (end of 2021)

Licensing partner announced

Revenue recognized (not till 2023)

Were this a private venture opportunity, this would strike me as a very attractive risk reward. Yet, this is now publicly traded. This will be a fascinating company to follow through the coming years.

Other notes and sources:

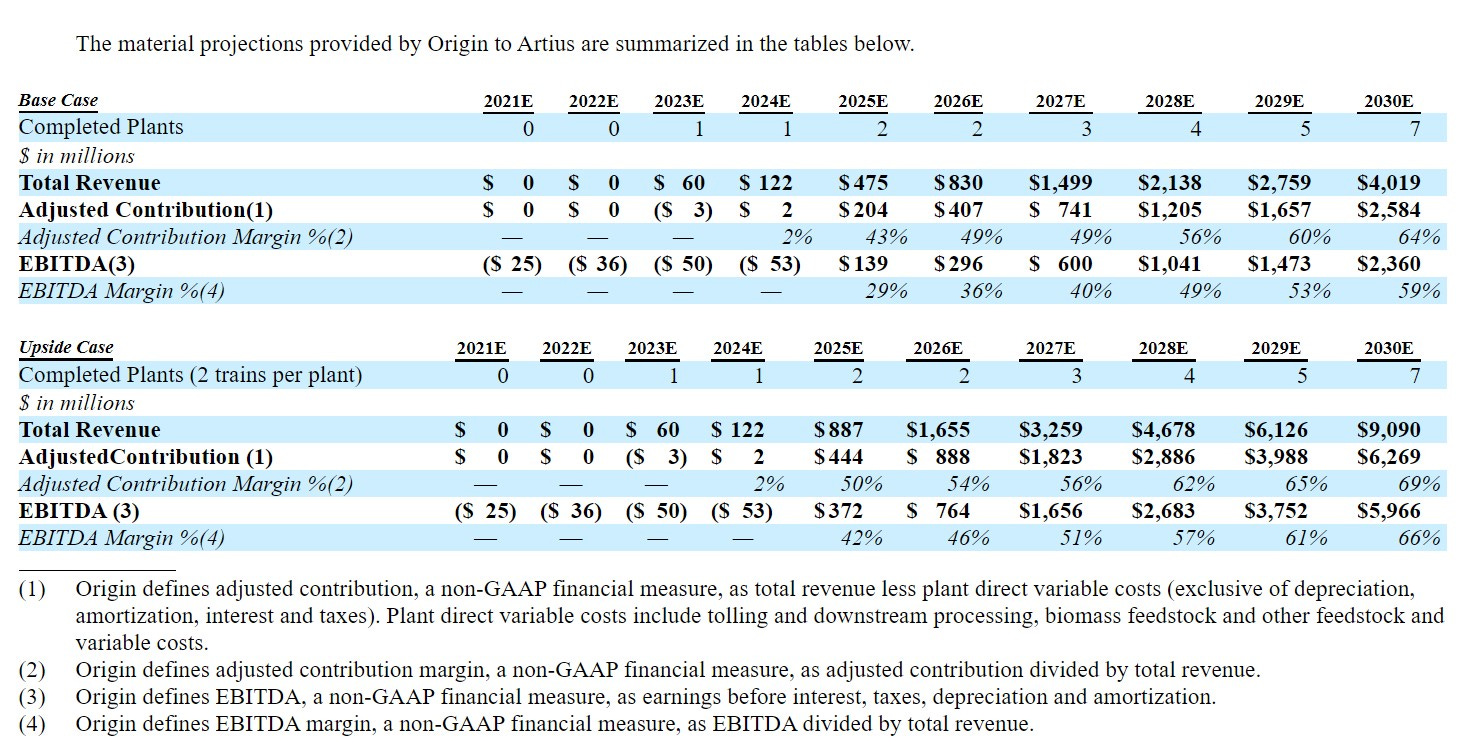

Original financial projections below for reference [Prospectus, page 117], but I’m not really putting any weight on it. This either works, or it doesn’t work.

The ValwithCatalyst twitter account had incredible invaluable information on this opportunity. It included a link to an excellent Value Investors Club writeup as well as to the below video which goes into depth.