Sprouts Farmers Market

Sprouts Farmers Market

A healthy business ready to restart growth

Note: For entertainment and informational purposes only. Not investment advice. Please do your own research.

Summary

Sprouts Farmers Market (ticker SFM) offers a farmers market grocery experience with a focus on fresh and healthy foods sourced locally at an excellent value. After going public at $18/share to great fanfare in 2013 (first day close at $40+), the company has seen multiple leadership changes, leaned on debt expansion to fund growth and share buybacks, and endured a languishing stock (currently <$25). After Jack Sinclair (ex Walmart) joined the company as CEO in 2019, the company has reset its strategy, repaired the balance sheet, invested in its fresh supply chain, and is now poised to resume opening new stores. Management is targeting 10%+ annual unit growth and sees a path to double its footprint of ~360 stores today. The company has consistently produced operating cash flows >$300M+ and trades at <$3B market cap. While it operates in a competitive and slow growth business, the company has a differentiated customer proposition, a long growth runway, and generates enough cash to both allocate capital toward growth while also buying back a lot of shares. I see a case for the stock to appreciate ~3x-5x+ in the next 10+ years.

Contents:

Introduction

Investment Highlights

Sprouts Long-Term Strategy

Leadership

Competition

Q2’21 Performance was Underwhelming

Valuation Thoughts

Risks

Conclusion

Introduction

Peter Lynch had three key rules to investing:

Only buy what you understand

Always do your homework

Invest for the long run

He outlined 6 categories of stocks. His favorite was the Fast-Growers category, stocks that were small, moderately fast-growing companies that could be purchased at a reasonable price. The best expression of this was often in retail where once a concept was proven out in a particular region, it could be scaled across the country, providing tremendous visibility into the pathway for growth.

Sprouts is not quite a Fast Grower, but it’s a company that has been growing well for its industry, which is rightly perceived as boring, low-growth, low margin, and intensely competitive.

I’ve been shopping at Sprouts since the first store opened in the area around 2010. It’s part of a regular rotation for us, which includes Costco, Whole Foods and Trader Joe’s.

It’s a stock that I’ve been eyeing for many years, but it’s finally at a point where I think the entry point is attractive.

Investment Highlights

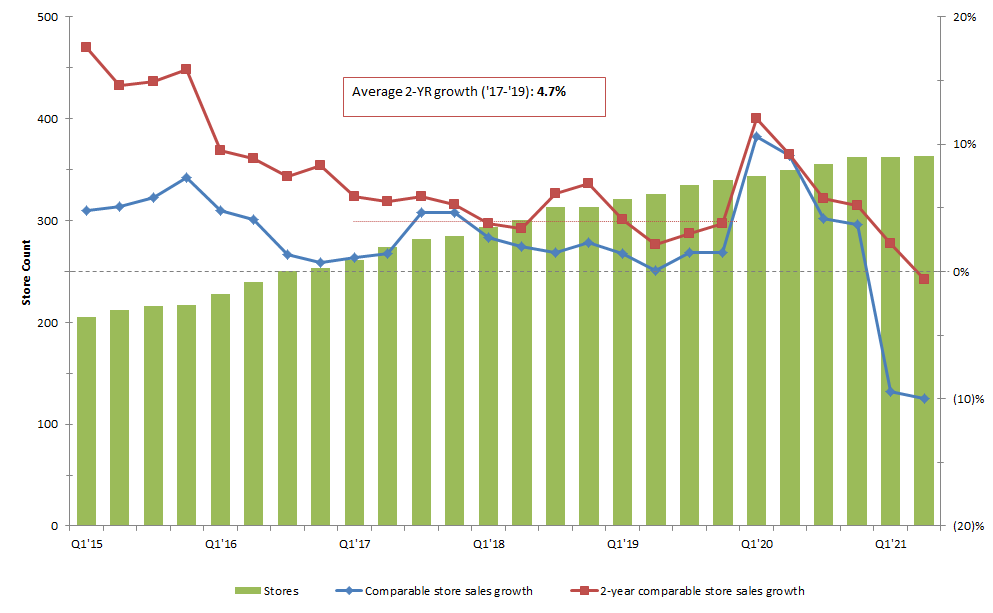

The business has been remarkably consistent. Revenue has grown at a 10% compound annual growth rate (CAGR) over the past 6 years from $3.6B to $6.2B in 2021 (H1’21 annualized). Gross margins have been in the mid 30% range, return on invested capital (ROIC) in the low teens, and operating cash flow margins around 6%.

The company has expanded the store count significantly since 2015 - from 205 stores to 363 stores as of Q2’21 - while maintaining decent same sales store comps. This also represents a CAGR of ~10% for that period. The company in fact had yet to experience a quarter of decline of comparable store growth until 2021, likely due to the COVID bump in 2020. Taking a more normalized view of performance (e.g., 2017-2019) suggests same store sales growth of ~2% to 3%.

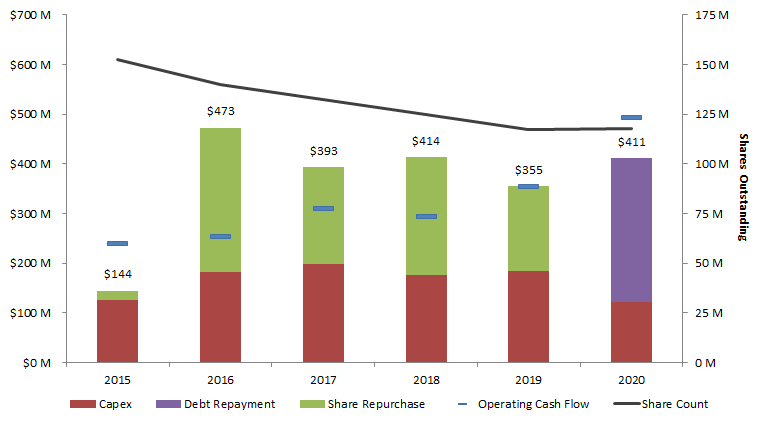

The company got a bit ahead of itself in capital allocation in 2016-2018, spending more on share repurchases and new store openings than what they were generating in operating cash flow.

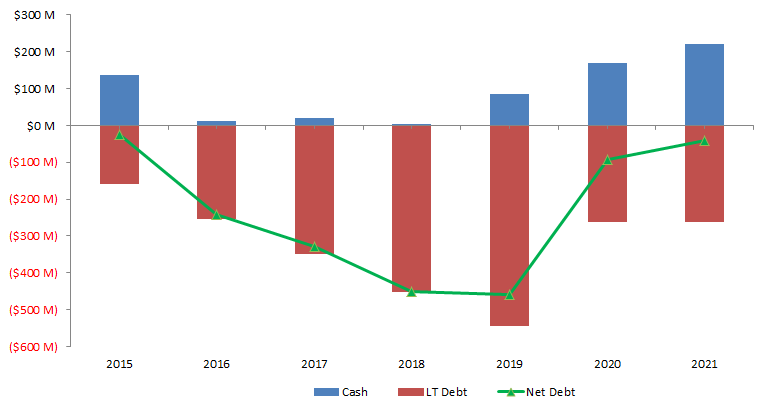

This was funded primarily by taking on increased debt starting in 2016 and peaking in 2019. In fact, the cash balance was quite minimal for these years, though the company was never really in serious trouble. Since Sinclair came on, the company has started to pay down its debt and has returned to a much healthier net debt balance. They paused share repurchases in 2020 in favor of paying down debt, but they recently restarted their buybacks in Q2’21.

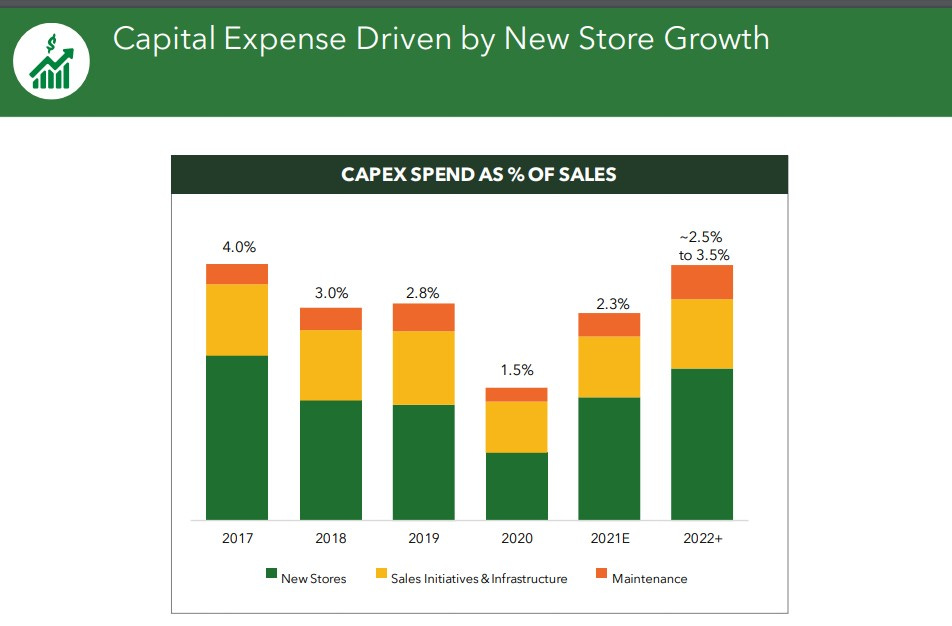

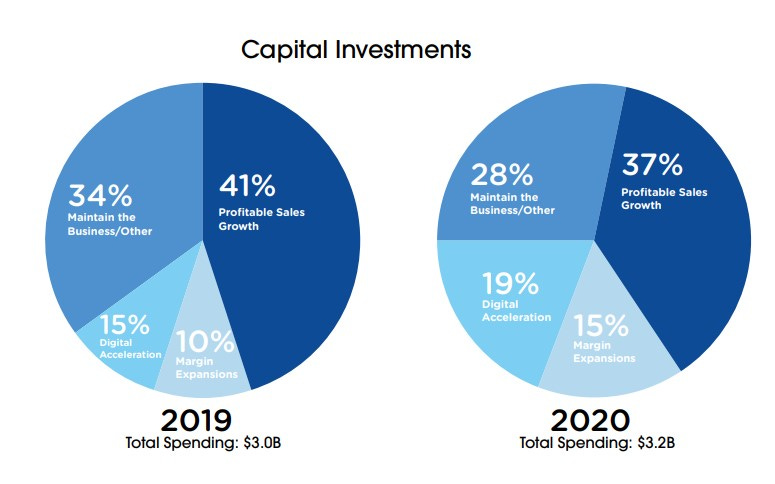

Most capex spend is devoted to growth vs. maintenance. See their investor presentation (Aug 2021) below.

The is in contrast to the mainstream grocers. Kroger, for example, has a different capital allocation given their much larger and mature footprint. It’s less about opening new stores, and more about optimizing their existing ones. The ‘Profitable Sales Growth’ category is primarily store remodels and merchandising initiatives that are specifically linked to Kroger’s 2-4% annual identical store growth goals.

Source: Kroger 2020 Fact Book

In my view, the ~70% of Kroger’s capex spend related to ‘Digital Acceleration’, ‘Margin Expansion’, and ‘Profitable Sales Growth’ roughly ties to what Sprouts deems ‘Sales Initiatives and Infrastructure.’

I’m more inclined to view those efforts as necessary upgrades to keep pace, rather than true sources of new growth.

Overall, I estimate the growth vs. maintenance capex split to be 2/3 vs 1/3. In other words, Sprouts spends ~3% sales on capex, with ~1% going to maintenance, and ~2% going toward growth.

Sprouts has a lot of room for expansion. The long potential growth runway is the key differentiation relative to the other public grocery companies.

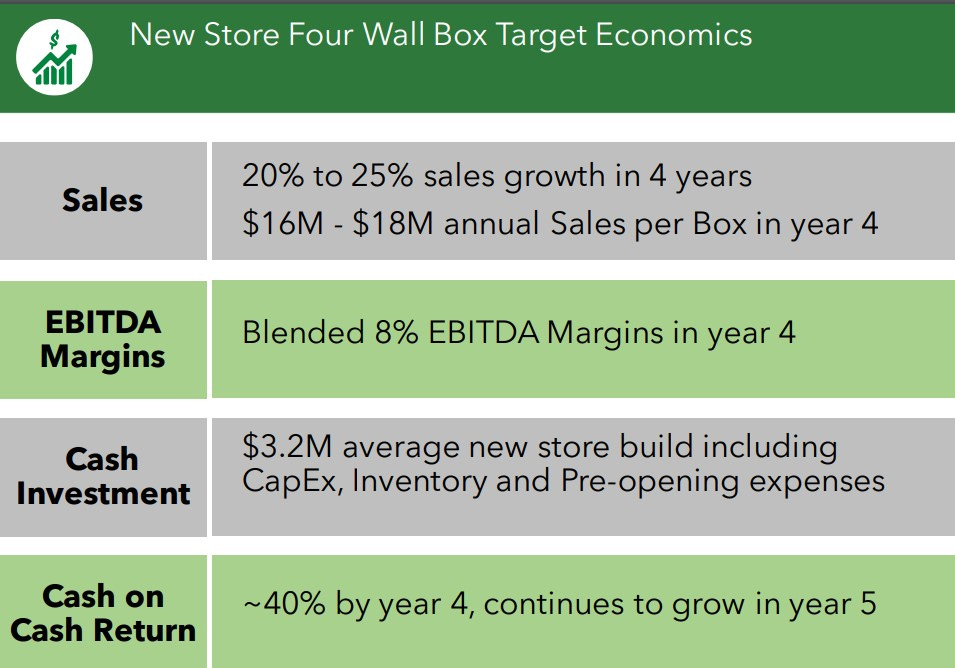

There is a solid ROI in opening new stores, and they have ample cash generation to fund this growth. The company is currently shifting to a new smaller store format (21k to 25k square feet), compared to their current 29k average. Management expects the typical new format store to cost ~$3.2M to open (saving 20%). They expect the store to generate $17M annual sales with 8% EBITDA margins by year 4, or ~$1.4M in EBITDA per store. These assumptions still need to be validated as the first new format smaller store only recently opened.

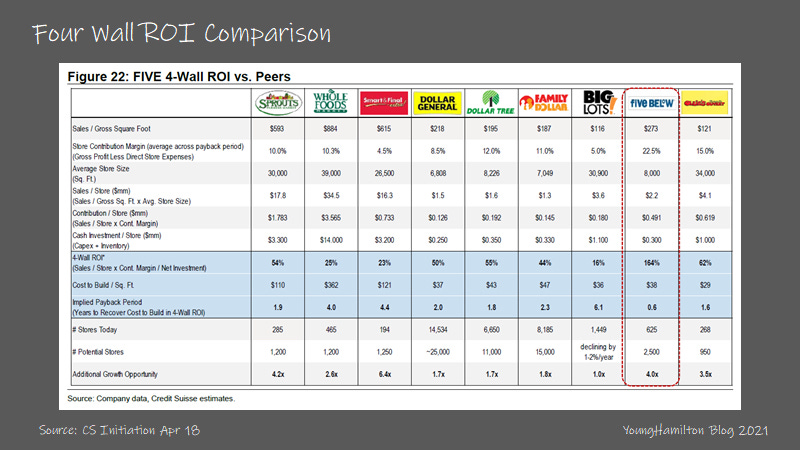

The following chart from the Young Hamilton Analyzing Good Businesses substack focuses on Five Below and is a bit dated, but I found the Sprouts and Whole Foods metrics instructive. Specifically, it costs 4-5x more to open a new Whole Foods vs. a Sprouts.

Even assuming $4-5M to open a new store, the company could open 20-25 new stores per $100M in capex spend. This could be funded based on the operating cash flow as indicated earlier.

2021 has been a year to establish the foundation to support their future growth, primarily in opening two distribution centers in their Colorado and Florida markets. Colorado appears to be about improving efficiency while Florida is an expansion market. They will also be opening a new distribution center to support their expansion in PA/NJ/MD area. Management has indicated that they expect to restart 10% unit growth starting in 2022, and they seemed primed to do that.

Retailers that have developed a solid and profitable unit concept that can be rolled out efficiently at scale have typically done pretty well during their growth expansion phase.

Sprouts Long-Term Strategy

In Q2 2020, shortly after Sinclair joined as CEO, Sprouts put out a revised strategy deck for 2020 and Beyond. The following slides are taken from their latest investor deck (Aug 2021):

They are targeting Health Enthusiasts and Experience Seekers who care about fresh, natural and organic food options. This spans across incomes and age demographics.

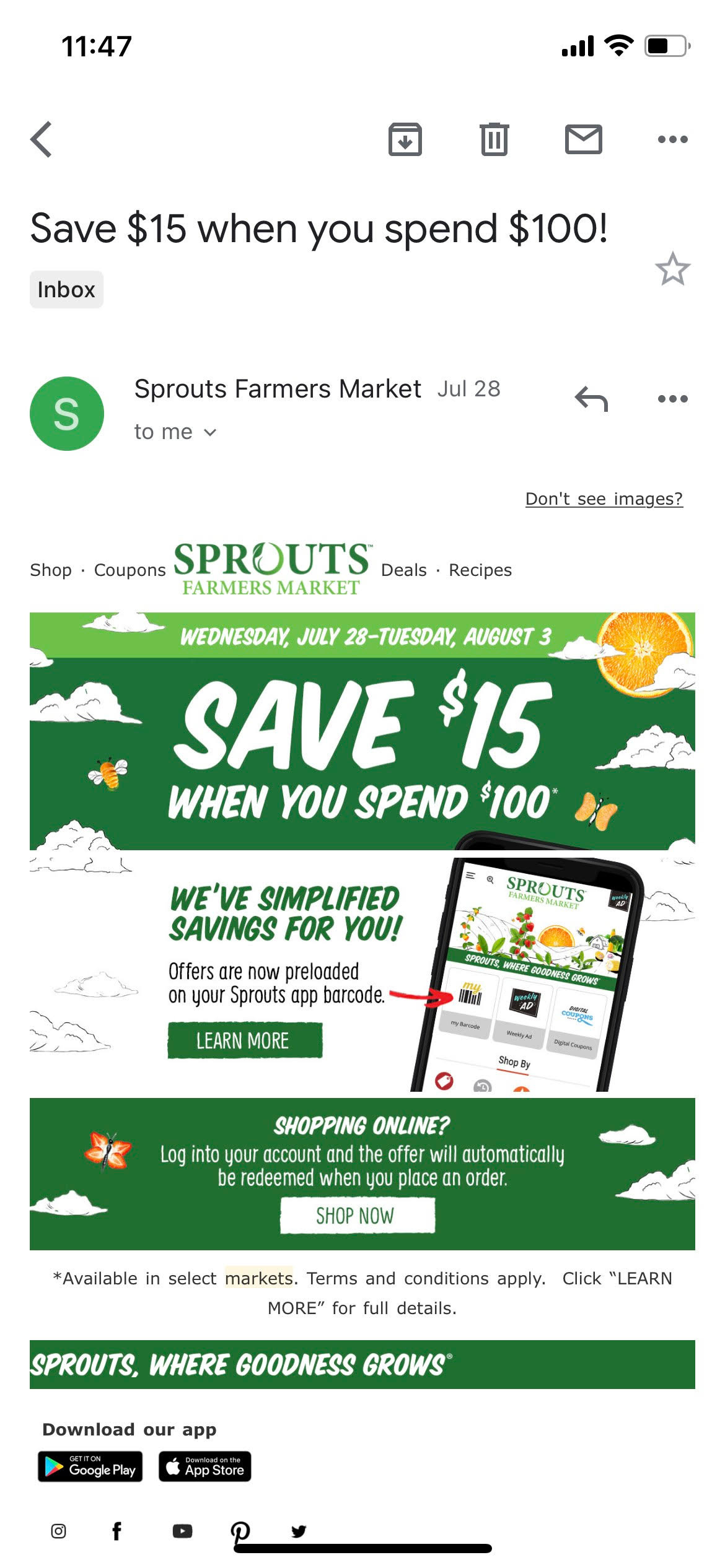

They are moving away from inefficient loss-leader customer acquisition strategies in favor of better optimization and ROI. They used to promote weekly loss-leader specials (e.g., 10 for $1 corn) that were marketed via physical mailers. These used to be released on Wednesdays and could be stacked, so I would make an effort to go to Sprouts specifically on Wednesdays.

The company has since pivoted to a digital-first marketing platform and has backed away from these specials. The coupons I receive now come via email and are geared toward promoting larger basket sizes ($15 off $100) or highlighting their differentiators (e.g., 25% off organic produce).

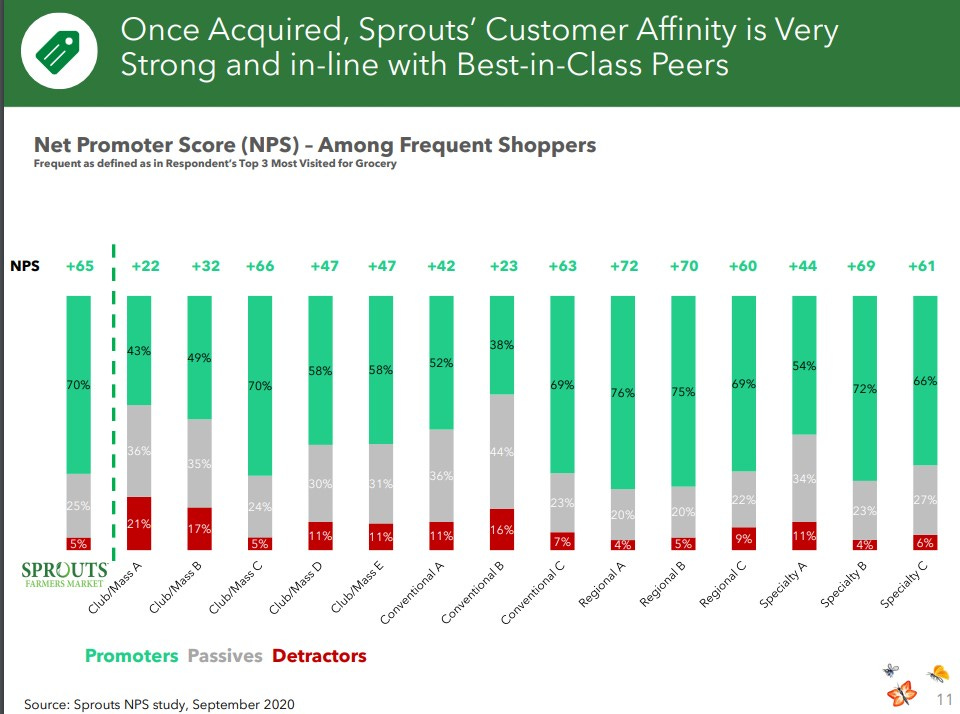

They still have a ways to go, but once Sprouts attracts a customer, they do seem to score well relative to other grocery options.

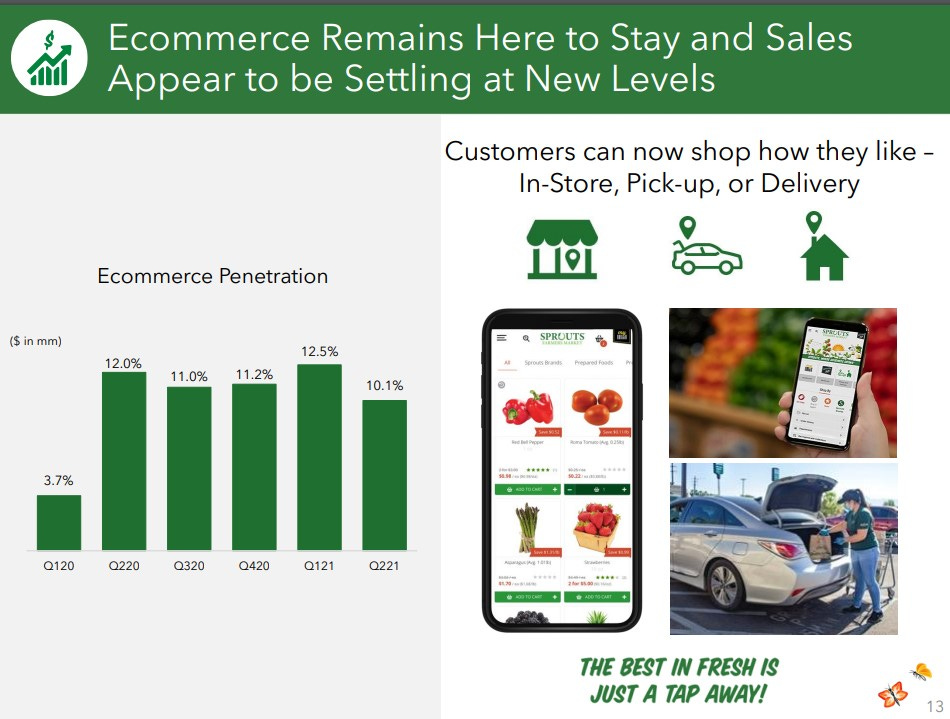

They also rolled out their e-commerce capabilities during COVID via Instacart. I’ve used it a couple times but prefer to shop in person. Sprouts charges a nominal fee ($1.99) for pick-up. E-commerce penetration appears to be settling around ~11%.

But the key is that Sprouts’ product assortment is differentiated and local. 68% of items are attribute driven per the below slide. I can’t find anything in Sprouts from the large processed food companies (e.g., PepsiCo, Nestle, General Mills, etc.). There are also entire sections - vitamins, bulk grains/nuts/spices - that we no longer use.

They are also improving their operations by reducing the footprint for new stores from 30k to 23k square feet, while also opening two new distribution centers in FL and CO to increase their fresh supply chain coverage and locate stores <250 miles.

While seemingly obvious, this was not always the case. The WA stores for example are still on an island relative to the rest of the DC network. I could see this approach and focus on fresh and local products eventually creating slight process, cost and supplier relationship advantages within specific regions.

The below video describes the 135k Aurora CO distribution center which will support 45 stores across Utah, Colorado, and New Mexico.

Sprouts strategy in summary:

Win target customers through their refined brand and marketing efforts

Expand the store count with the new smaller format

Improve the supply chain and distribution center system for efficiencies and to offer fresh and local products

Reinvest to fund 10%+ unit growth and use the rest of the cash to repurchase shares

Leadership

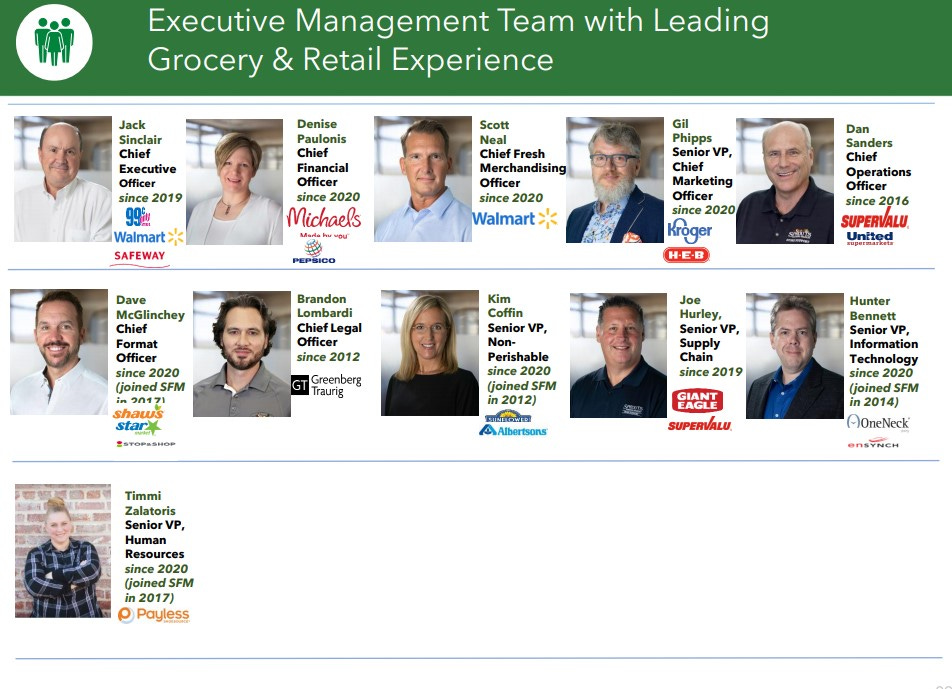

Under new management. Jack Sinclair was brought on as CEO in 2019. He previously was EVP US Grocery for Walmart from 2007 to 2015 and also spent 14 years at Safeway. The other C-level executives have impressive and relevant backgrounds as can be seen below. The key takeaway is that almost all of them joined in 2020.

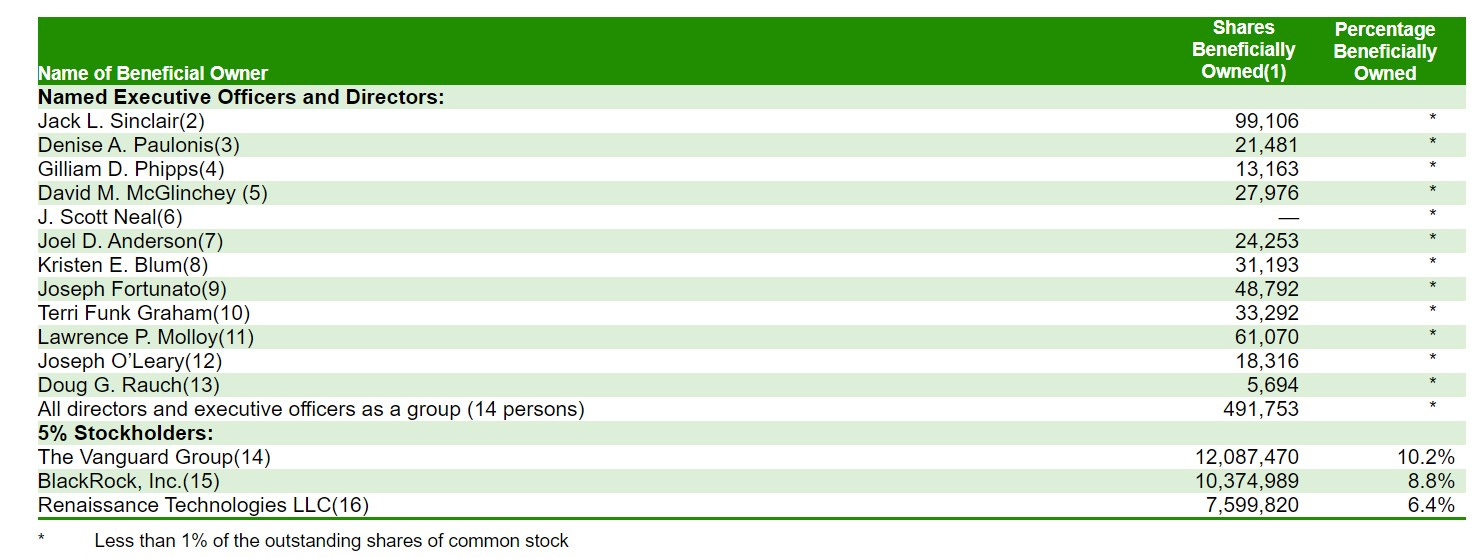

Unfortunately, that means management currently doesn’t own much stock in Sprouts, at least not yet. From the 2020 Proxy statement:

However, the company does have stock ownership guidelines:

Within five years of appointment to their position, our Chief Executive Officer must obtain and maintain beneficial ownership of shares of Sprouts stock equal in market value to five times his current annual base salary, and our other executive officers must maintain beneficial ownership of shares of Sprouts stock equal in market value to two times his or her respective current annual base salary.

Management is incentivized by a performance based cash bonus based on: pre-tax earnings (75% weighting) and comparable store sales growth (25% weighting). 2020 was a huge year for these execs, as they earned 3x of their performance bonus.

The Board also appears solid and relevant, with 7 of 8 directors independent, and board members having average tenure of 5 years.

The chairman Joseph Fortunato was formerly the CEO of GNC.

The rest is a mix of operators (CEO of Five Below, President of Trader Joe’s, President of PetSmart), tech (CIO of PepsiCo), marketing (CMO of Jack in the Box), finance (CFO Under Armour, PetSmart),

On the employee front, the company seems to be doing a solid job. They publish the following metrics in their 2020 ESG report.

Overall, the leadership looks good to me, but I would prefer to see more skin in the game. I would like to see their ownership stakes grow over the coming years.

Competition

In the U.S., there are ~40,000 grocery stores. Below are the largest names:

Walmart: 4,200

Kroger: 2,700

Albertsons (Safeway, Albertsons, and Vons): 2,300

Publix: 1,200

Ahold: 1,900

Aldi: 2,500

Whole Foods: 500

Trader Joe’s: ~550

Costco: ~550

Not on this list is Sprouts and its 363 stores.

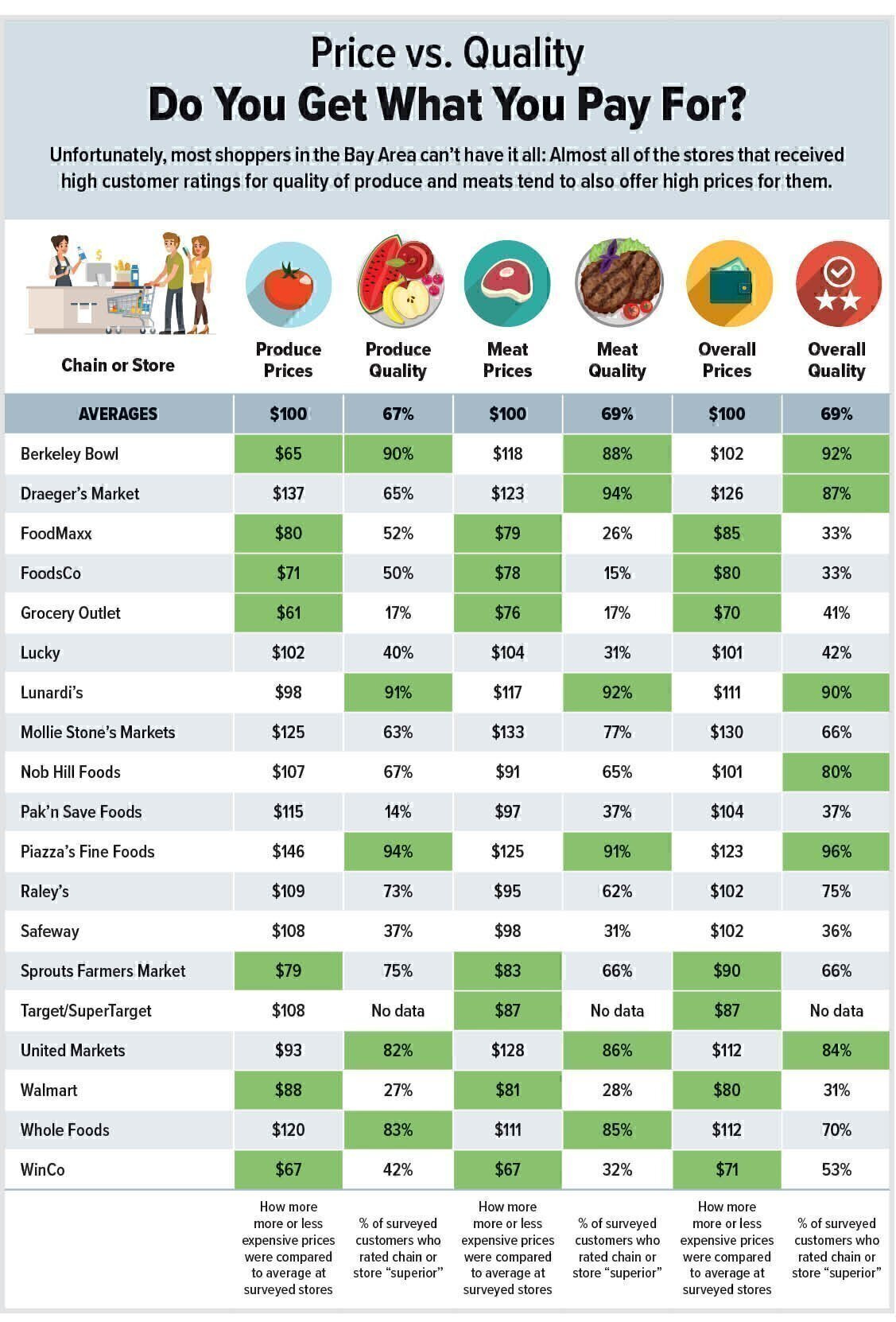

Grocery is a notoriously competitive and low-margin business. To illustrate, the following table from Checkbook assesses local grocery stores in the Bay Area. Sprouts is slightly better than middle-of-the-pack overall: decent quality at good prices. While a solid choice, it doesn’t really stand out in any dimension.

The above chart also excludes Sprouts’ most relevant competitor: Trader Joe’s.

While their assortment is different, Sprouts simply does not inspire the same loyalty or crowds that Trader Joe’s does. Regrettably, Trader Joe’s is private and not available for investment.

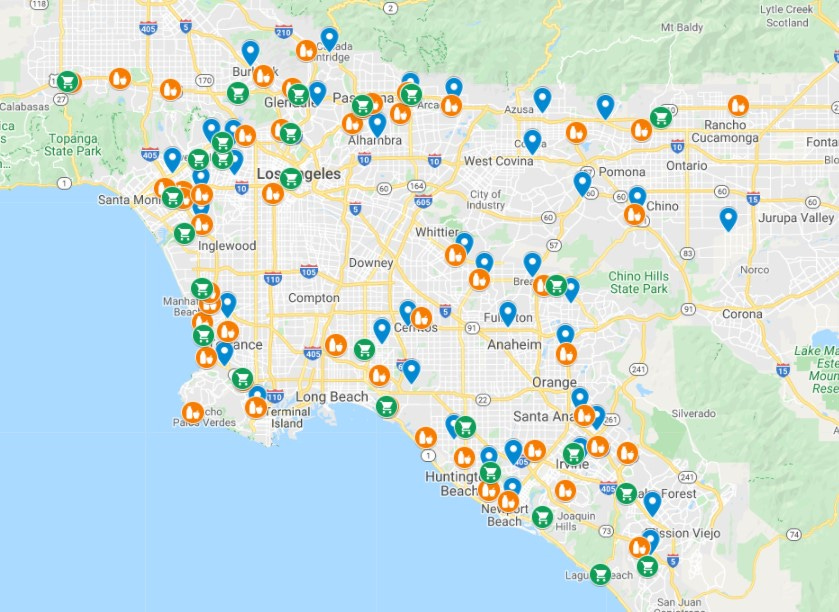

But that may be ok. Below is a map of locations for Sprouts (blue), Trader Joe’s (orange), and Whole Foods (green) in the Los Angeles / Orange County area.

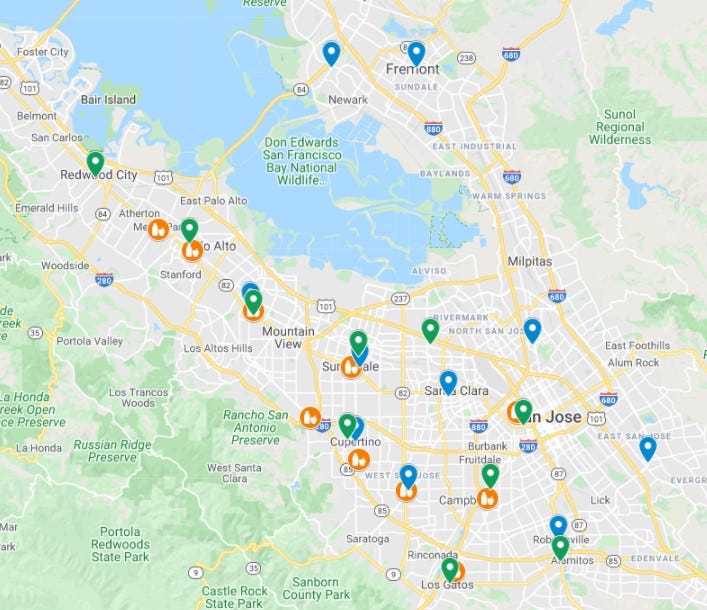

This is what it looks like in the Bay Area (South Bay).

It always seemed to me that Sprouts and Trader Joe’s seemed to cluster together, and the above maps would appear to confirm that observation.

Many of these Sprouts stores have been open for a number of years. The proximity of Whole Foods and Trader Joe’s does not seem to have negatively impacted Sprouts’ overall comparable store growth numbers in the past. The bottom line is that their stores and locations do not appear to be at risk of oversaturation for awhile.

As a shopper, I go to Sprouts several times a month and spend several thousand dollars a year with them. I also visit Trader Joe’s, Costco and Whole Foods regularly as well. The below reflects my perspective as a shopper. I note that my behavior may not reflect the habits or preferences of the general population.

Trader Joe’s assortment is truly unique with more than 80% private label. The best deals are in processed foods, snacks, and alcohol. We typically don’t buy produce or meats there.

Whole Foods is called “whole paycheck” for a reason, where you (over)pay for the quality, except their private label items. The interior is pristine, but it feels increasingly impersonal with the proliferation of professional shoppers.

Costco has limited bulk selection and is excellent, but not the place for produce or perishables. This is a bi-weekly stop for staples.

Sprouts typically offers the best value x quality trade-off for fruit, vegetables and meat. It has decent private label items (e.g., organic milk, eggs, healthy snacks). Sprouts also tends to be less crowded compared to the others.

We generally stay away from the mainstream grocery stores.

As a grocery store, Sprouts is simply solid, and nothing too spectacular.

The one area where it does stand out is in financial performance. I put together the following comparison table from Kroger’s 10-K and Whole Foods last 10-K from 2017.

Kroger defines ‘Fresh’ as produce, floral, meat, seafood, deli, bakery and fresh prepared. Sprouts defines ‘Perishable’ as produce, meat, seafood, deli, bakery, floral and dairy and dairy alternatives.

Whole Foods has somewhat surprisingly not done that well since its acquisition by Amazon in 2017. Amazon doesn’t break out Whole Foods separately but lumps it in with Physical Stores. Sales have basically been flat to slightly down since 2017. Given how Amazon operates, it wouldn’t be surprising if operating margins have trended down as well.

On a per unit basis, Sprouts seems to hold its own compared to Whole Foods. On a sales basis, the average Whole Foods store pre-acquisition did ~2x the volume of a Sprouts store (~$17M). However, Whole Foods uses a larger footprint and is more expensive to launch and operate. On an operating income basis, the gap is not as large. As Sprouts continues to reduce its average store size with the new format (which supposedly will have comparable sales), the average Sprouts store may eventually contribute as much if not more cash flow than the average Whole Foods store.

Kroger has invested a lot into its digital initiatives and recently broke into the top 10 in online sales, but online is still a lower percentage of sales compared to Sprouts. Their margins are lower, though their private label percentage is higher. They also have more debt and not as many new store expansion opportunities for growth.

Sprouts meanwhile has excellent margins, a stronger balance sheet, and a clear line of sight for growth. Arguably, there are opportunities to improve margins further given the improvements from supply chain and marketing to be realized as well as the relatively lower percentage of sales coming from private label goods [Statista].

Provided it can maintain its performance, the outlook for Sprouts looks pretty good. That is the caveat, however.

Q2’21 Performance was Underwhelming

Sprout's Q2 earnings release (presentation, transcript) in early August, and the financial results were not great. Management pointed to the dynamics of re-opening coming off last year’s COVID spike as the reason. Customers were traveling and dining out again, which affected their sales.

Comparable store sales growth: (10.0%)

2-year store sales growth: (0.6%)

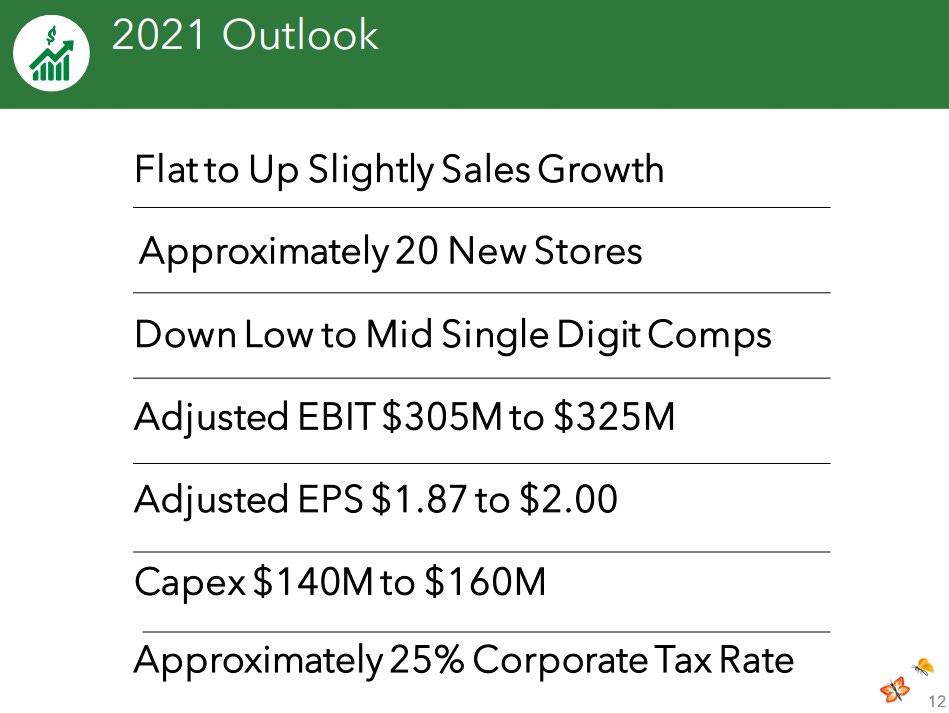

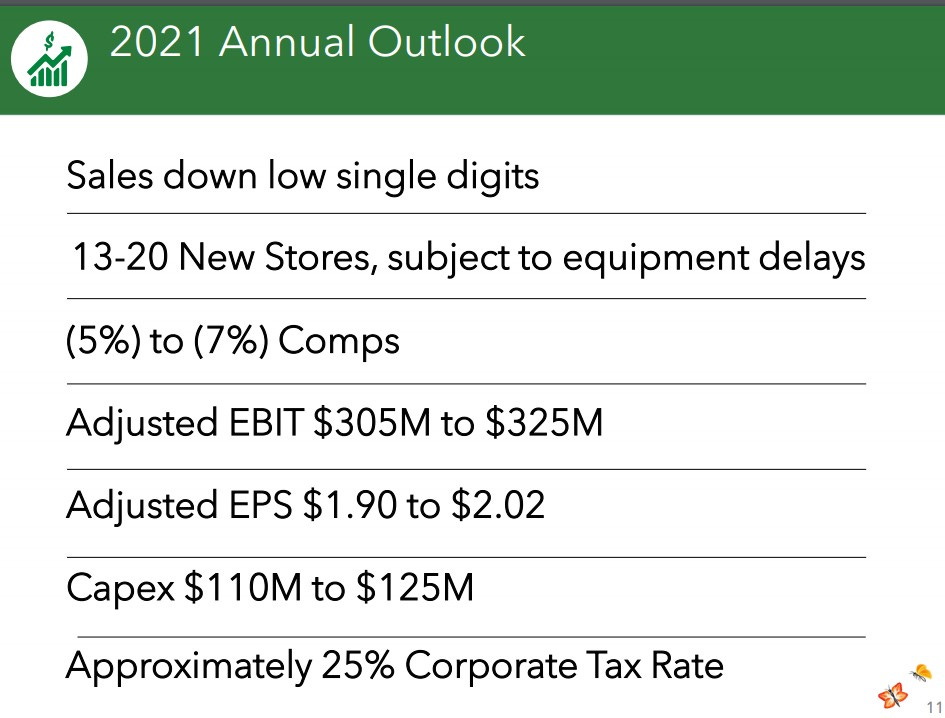

Reduced 2021 guidance pretty significantly:

Sales Growth: “Flat to Up Slightly” to “Sales down low single digits”

New Stores: “~20 new stores” to “13-20 new stores”

Comps: “low to mid single digit” to “negative 5% to 7%”

Prior outlook at Q1’21:

Revised outlook lower for Q2’21:

On the other hand, some of the the operational parts showed promising signs:

Distribution centers: Launched both of their new DCs in CO and FL (June). More than 85% of stores are now within 250 miles of DCs

New format stores: 2 new format stores opened in Q2, with plans to open 3 more in 2021.

Marketing: This was mixed given the financial results. The brand and marketing efforts were noted to have increased awareness and purchase intent, but hadn’t yet translated into increased traffic or actual purchases. This would be the next step, but they are staying the course.

More importantly, the company started repurchasing shares. They spent $87M toward the end of Q2 (average price $26.75), and another $25M after the end of quarter. They still have ~$188M in repurchase authority remaining out of the $300M repurchase authorization they announced in March.

Given their first half operating cash flows was $177M, it’s possible they could exhaust that remaining authority by the end of the year. If so, and depending on their stock price, they will likely end the year at under 108M shares, down from 114M currently, and from 118M at the start of the year. That would represent a ~9% reduction in share count. We’ll see whether or not that happens.

Given the massive cut in outlook, I would have expected a negative reaction in stock price, but that didn’t seem to be the case. The stock traded relatively flat.

However, compared to the other grocery companies, the recent divergence in stock performance since the last quarter’s earnings is notable:

Sprouts has basically been flat the last year, while both Kroger and Albertsons saw dramatic spikes. Very dramatic in the case of Albertsons.

Albertsons also had a (10%) decrease in identical store sales growth following their July earnings release, but they raised their 2021 outlook:

Identical sales: (5%) to (6%), previously (6%) to (7.5%)

2-year stack growth: 10.9% to 11.9%, previously 9.4% to 10.9%

Quarter end: June 19, 2021

Krogers saw a (4.1%) decrease in identical store sales growth following their July earnings release. They also raised their 2021 outlook:

Identical sales: (4.0%) - (2.5%), previously (3.0%) - (5.0%)

2-year stack growth: 10.1% - 11.6%, previously 9.1% - 11.1%

Quarter end: May 22, 2021

The key difference seems to be the revised annual outlook: the upward revisions were fairly minor, but Sprouts’ downward revision was major.

This is most likely unique to Sprouts, but it’s possible there may be market-wide effects. In the Sprouts call transcript, management offered the following color around timing of the weakness:

“While April experienced strong results both top and bottom line, we were disappointed with May and June.”

Sprouts announced earnings on August 5, while Albertsons announced on July 29, and Kroger on June 17.

Given the odd quarter end dates for Albertsons and Krogers (which happened earlier than Sprouts), I wonder how much the difference in sales performance was due to different time periods. However, it did not seem to affect the 2021 outlook that they provided.

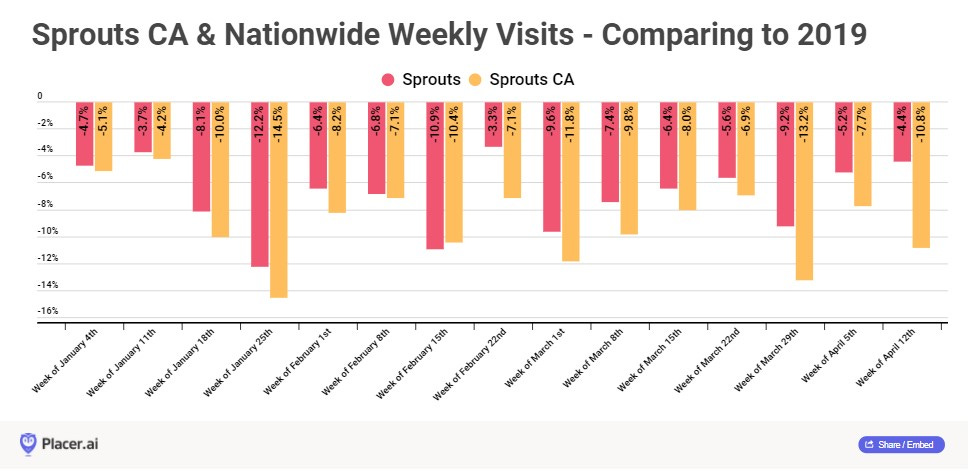

In general, the reopening hasn’t been as kind to Sprouts as to the other grocers. Placer.ai has some interesting stats in a post on Sprouts’ traffic in early 2021 - negative and more negative in California:

The silver lining pointed out in that post is that CA had been slower to reopen relative to the rest of the country during that time, and Sprouts is overly concentrated in CA.

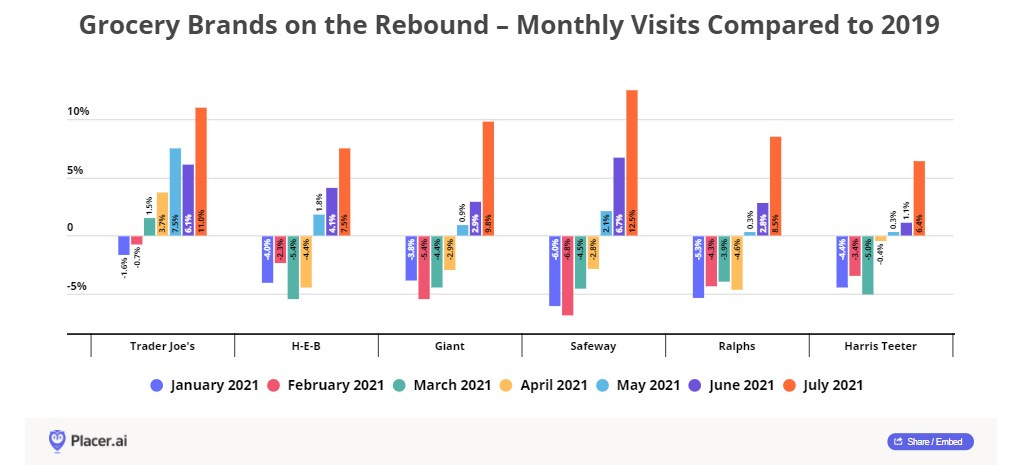

For the other grocers, there has been a noticeable recovery:

Most of the grocers saw a large uptick in traffic compared to 2019 starting in the summer months. It’s possible that this will all correct itself in short order.

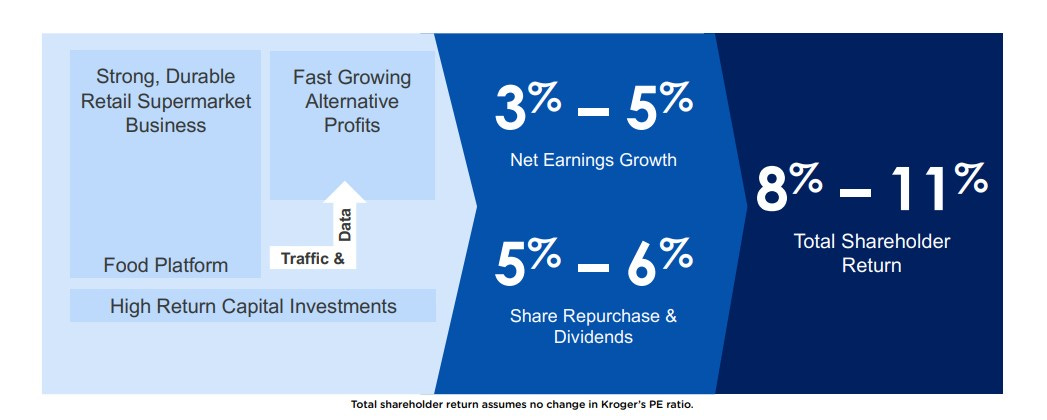

Grocery had been trading at attractive multiples earlier in the year. Berkshire Hathaway has been building a position in Kroger, and now owns 8% of the company.

I’ve been evaluating Kroger to understand why, but I end up concluding that Sprouts is the more attractive opportunity for me. As mentioned earlier, Kroger appears to be mostly spending to remodel and optimize existing stores rather than launching new stores, and it has much more debt. It’s tough to grow from such a large base, and most of its increases in store count has come via acquisition. That may actually bode well for Sprouts down the line.

Kroger is definitely targeting a decent total shareholder return per below [2020 Fact Book] and the stock has already had meaningful price appreciation, so what do I know?

Valuation Thoughts

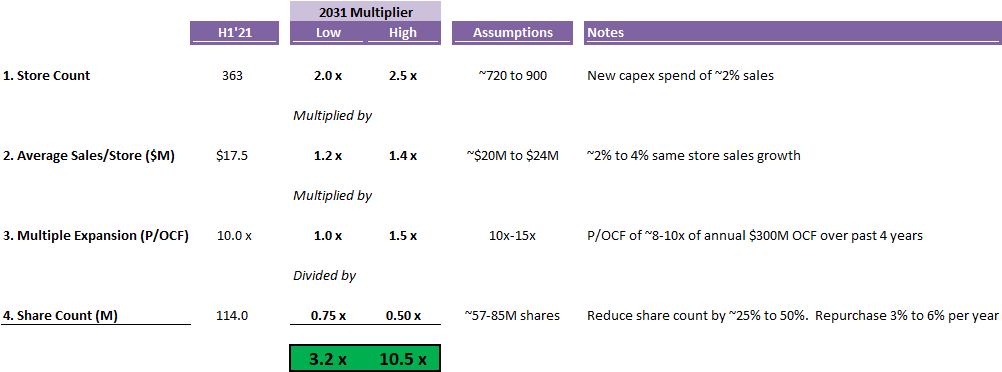

I believe there is a 10+ year runway of growth for Sprouts, primarily through continued new store expansion.

There are four key variables and assumptions in my view:

Store count. How many stores can this grow to from current store count of 363?

Comparable store sales growth. How much sales will each store produce?

Multiple expansion. Will SFM continue to trade at its current multiple?

Share count. How many fewer shares will there be in 10 years?

The low case assumes that in 10 years, store count doubles, average store sales increases by 20%, the multiple stays the same, and the share count is reduced by 25%. That results in a roughly 3x outcome.

Reducing shares by 25% over 10 years implies that Sprouts repurchases ~3% of shares outstanding per year. I think they could actually do a lot more than that, as they’ve already retired 4% of shares in H1’21 alone). If the stock continues to stay depressed, then the impact of the share repurchases will be more pronounced. Repurchasing ~6% of outstanding shares per year would cut the share count in half over 10 years. A 3-5x return over 10 years from here feels like a plausible outcome to me.

The high case assumes more aggressive growth in store count, average sales and multiple expansion, as well as the share buybacks. These variables affect one another though (e.g., multiple expansion will affect the number of shares repurchased), so the upside is more uncertain. I indicate the assumptions to achieve a 10x return in 10 years, and I do think it is a real possibility.

That assumes the following:

Margin profile continues to hold. Any deterioration in the business will obviously weaken the reinvestment flywheel.

Capacity to expand is not affected by competition or new consumer grocery buying behavior

Execution to expand store count by 10% per year efficiently.

The wildcard is if the narrative around the company changes, and Sprouts inherits the Whole Foods mantle as the leading pure play organic food retailer, resulting in a much richer multiple. This is yet to be widely accepted by the market, and it ultimately may never happen.

I believe there is the cash and the execution to continue launching 30-40 stores per year for many years to come. I feel shaky in the consistency of the margins, but I was pleasantly surprised to see their historical performance. I am also encouraged by the company recent initiatives (e.g., locating fulfillment centers closer to stores) which would seem to suggest that further margin improvement is possible.

Simple, stable, high cash flow businesses with feel-good stories and long reinvestment runways where most capex is devoted to growth shouldn’t trade at ~10x operating cash flow in this interest rate environment. Grocery stores are also essential businesses and theoretically act as inflation hedges (provided prices can be passed to customers).

The annual growth is not eye-popping, but Sprouts is still likely to grow 10%+ per year for years to come.

That takes us to how the stock has traded.

Sprouts went public on Aug 6, 2013:

Priced at $18, closed first trading day at $40.11

163 stores in 8 states at the time, mostly in the Southwest

~150M shares

Since 2013, they’ve more than doubled their store count, maintained their margins, and cut their outstanding share count by ~25%, but the stock has basically been on a steady multi-year decline. It has recently leveled off a bit though.

Nick Sleep (Nomad Investment Partnership letters) famously concentrated his investments into scale-economies-shared businesses Costco, Amazon and Berkshire Hathaway.

He first wrote about Costco in 2002. Some of the details about Costco at the time bear a resemblance to Sprouts:

The density coast to coast implies room for around 1,000 US stores (currently 284)

At 10% growth per annum, this implies the firm has another 13 years of growth ahead

The share price has declined from a year 2000 high of U$55 to U$30 (Nomad’s purchase price) as margins declined slightly (they are measured in basis points at this firm) with the cost of several new distribution centers which will support the next few year’s growth.

At U$30 the firm is valued as a cash cow, with higher levels of profitability (as capacity utilisation increases) and modest levels of growth justifying a valuation over U$50 per share. Costco is as perfect a growth stock as we have analysed and is available in the stock market at a close to half price.

I should clarify that Sinclair is not Sinegal (Costco’s CEO) and Sprouts does not enjoy an indomitable scale-economics-shared business model like Costco. Sprouts doesn’t even have a loyalty program (yet). There are similarities in the growth opportunity profile, but that’s where it ends for now.

Risks

In the bear case, the company’s poor Q2 performance represents the start of the decline. They fail to attract a core loyal customer base. The concept isn’t differentiated enough and doesn’t work - the store footprint is too small to be a one-stop shop, healthy organic foods are available elsewhere, and consumer behavior shifts to online. Consumers prefer to shop at fewer stores post-COVID, and Sprouts just doesn’t make the cut. The historical margins are unsustainable, and the company is unable to execute on its strategy of funding new store growth and buying back shares. The market continues to perceive the company as a no-growth play whose best days are behind it. Management turns over yet again or becomes susceptible to lowball M&A offers, as they aren’t truly owner operators. The company leverages up to pursue expansion or repurchases inefficiently. The stock price declines further and the company is eventually taken private at a rock-bottom price.

In the bull case, the company is successful in carving out a niche as the go-to successor to Whole Foods to cater toward health-conscious consumers at an affordable price. The company executes on its new store format and growth plans while maintaining if not growing its margins. Sprouts starts to cultivate a cost and efficiency advantages as well as network effects around local suppliers and their fresh regional supply chains. With their unique offering, Sprouts becomes an enticing and shiny acquisition target for larger players desperate for growth and ESG bona fides. If it stays independent, the company continues to grow its store count and retires a huge chunk of their outstanding shares. Management oversees a steady decade-long run of growth, accumulate a sizable ownership position, and eventually retire as the architects of a successful turnaround.

Conclusion

Based on Sprouts’ track record and initiatives in the works, I’m inclined to believe that Q2 was a blip rather than the start of a decline. My sense is that the divergence in stock performance following this quarter was an overreaction.

However, the company doesn’t really have any stand-out advantages. There is a slight case to be made for counter-positioning, brand, and local scale economies, network effects and process strength, but I’m not confident these are really durable advantages. The switching cost barrier just doesn’t seem that high for grocery.

I’ll be keeping an eye on the following milestones over the next few quarters:

New store format return on investment profile - do management’s assumptions still hold? There should be at least 5 data points coming out of 2021.

How quickly can new store counts expand? 10%+ growth would indicate 35-40 new stores in 2022.

Can they revive comparable store growth? Will we see evidence of the new marketing efforts working?

What is the impact to margins? Margins have been stable, but they are still higher than other grocers. Will potential inflation and competition supersede the positive effects of the distribution centers and other marketing initiatives?

Is management increasing their ownership stake? The current lack of management skin in the game prevents me from sizing up this position.

If they can sustain their margin profile and continue to grow their store count, then I think there is a strong case for a 3x+ return over 10 years. If they start to hit the conditions from the bull case, then I can see a much greater upside. The kicker is if the market starts to value cash flows more and rerates the stock higher.

Overall, I think this is a long-term hold that I can feel good about. I started building a position in the low 20s earlier in the year and plan to scale further (target 2-3%) while monitoring future performance.

Other sources: