Wish - Notes on the Quarter

Wish I knew what I know now...

Note: For entertainment and informational purposes only. Not investment advice. Please do your own research.

Wish’s second quarter was just shockingly atrocious. My prior thesis has effectively been shredded. They are not suspiciously undervalued anymore. The whole business model is suspect.

The bewildering part is that management seems to have been caught completely off guard by these developments. Peter pointed to a combination of re-openings leading to less user activity, unexpectedly high performance marketing costs leading to poor ROI, and slow app performance leading to a poor user experience.

It’s surprising how a company which had managed to compete effectively with Amazon and Alibaba for so long, which overcame seemingly overwhelming existential supply chain disruption issues during COVID, and which had convincingly billed itself as a strong data science / technology company, has managed to get so tripped up by this set of arguably foreseeable circumstances.

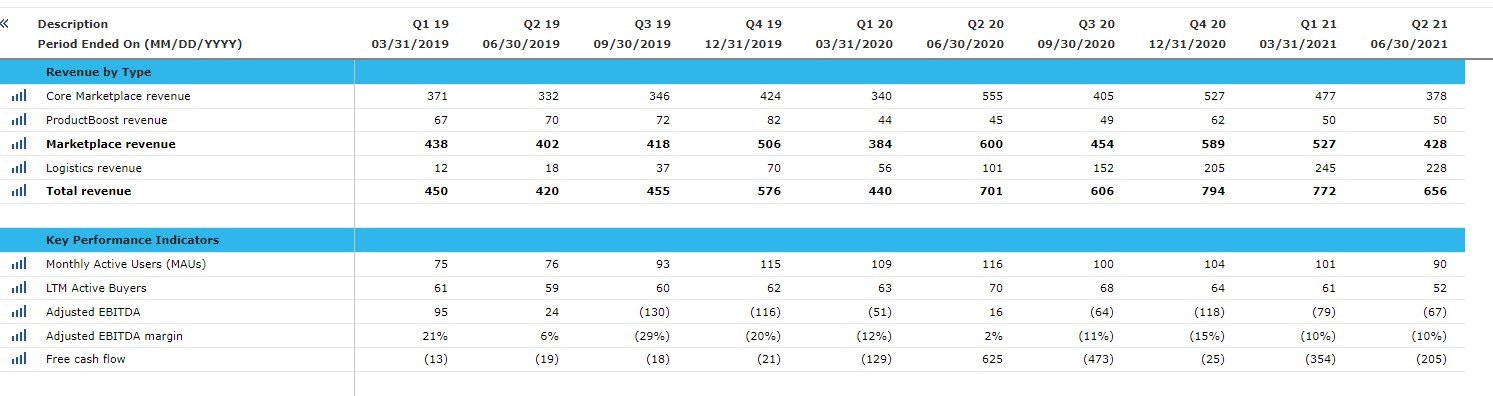

On the surface, the performance in the quarter doesn’t look that bad. A year-over-year revenue decline of 6% ($656M in 2021 vs. $701M in 2020) seems understandable coming off a tremendous Q2 2020 COVID result. It still far surpasses the $420M revenue from Q2 2019.

The problem is that core marketplace revenue has declined far more (29% down) than what has been made up in logistics revenue growth, which unfortunately is lower gross margin. The quarter apparently had “a strong start”, but then gave way to a massive decline that led to the underperformance.

Unfortunately, that negative performance shows no signs of abating. In lieu of providing Q3 outlook, Peter indicated:

Q2 MAUs were down 22% year-over-year and active buyers were actually down 44%, year-over-year. And this trend actually continued into July as MAUs are down 9%, even compared to June.

…to provide some context quarter to-date total revenue through July 2021 was down approximately 40% compared to the prior quarter, while marketplace revenue was down approximately 55% compared to the same period. With a pullback in digital ad spending, we expect third quarter revenue to decline further.

They are no longer confident that they can acquire customers profitably and so are cutting off new customer acquisition in favor of bolstering retention. While no formal Q3 revenue guidance was provided, the company was strongly hinting that the business was rapidly deteriorating and that Q3 would look to be about half of Q2 based on its current trajectory.

Even the quality of the shareholder letters between Q1 and Q2 was drastically different. It’s like they were written by completely different management teams.

What’s curious is that there were a number of positive developments coming into the quarter. They had announced several key executive appointments, including Jackie Reses as executive chair in May, and two former Google executives to become CTO and CPO in just the last few weeks. The company had been granted an EU Payment Services License in July, which provided an early hint at their payments ambitions.

I had thought their prior guidance for flattish growth in Q2 was an overly conservative estimate given their excellent past performance in order to provide buffer for lapping their breakout COVID quarter. Well, I was wrong in painfully spectacular fashion. Let me count the ways:

False Assumption #1: The business could be run for profit by turning off marketing. That was the first question in the earnings call Q&A. Management no longer stands behind that claim based on elevated advertising costs and a broken LTV/CAC customer acquisition model. That had been my key assumption to protect the downside - that this business could be run for cash if they stopped investing for growth. That can’t work when the business can decay so rapidly.

False Assumption #2: The business had resiliency given the high proportion of revenue from existing customers. Revenue from existing customers had been 70% of the business according to the IPO prospectus. Well, that can’t be true if your business can decline ~50% quarter over quarter.

False Assumption #3: The secret sauce of the business was in their data science and technology, as reflected in their functional headcount distribution and past performance. If that were true, then they would have caught and rectified their performance issues before it deteriorated to this level. At this point, it’s not clear that they have a viable business model.

The CFO resignation announcement toward the end of June now takes on an entirely different light. I had rationalized that departure at the time thinking that the company was actually looking to make a change, but should have realized the alarm bells when no replacement was announced. On the call, no update on the CFO search is expected until the end of the year. When the CTO and CPO joined in July, I assumed that their decisions reflected the earlier departure. Now I wonder how much they really knew about the company’s performance.

So what to do now?

What used to be for me a deep value long-term growth investment is now a speculative bet that this newly assembled management team can revamp the product and business model to staunch the bleeding and reinvigorate growth.

The downside protections have evaporated.

The cash balance is rapidly dwindling. There is still ~$1.6B cash, but they are now burning ~$200M a quarter.

Management no longer stands behind the claim that they can run the business at a profit by turning off marketing. The several years of FCF breakeven performance leading up to the IPO can no longer be relied upon.

Even with the marketing, metrics across the board - active buyers, revenue, gross profit - are declining by 20-50% across all geographies.

Unfortunately, there weren’t any good answers provided during the call to provide confidence that this decline could be halted in the near-term. It does not seem that the solution is known yet. The only logical thing to do is what the company is doing now: dial down spend significantly to diagnose the issue. That, however, has grave implications to growth.

I was discouraged that none of the new executives showed up on the call. When Reses joined as executive chair in May and had a brief appearance during the Q1 call, I was hoping that that she would be a constant presence and start to help tell the company’s story better. Unfortunately, there’s really no way to salvage this last quarter’s story. Her compensation package, which previously seemed so attractively performance-weighted, now appears hollow and provides hardly any incentive to stay.

The potential downside from here looks dire. It also, unfortunately, looks frighteningly probable. In this scenario, the company can’t figure out what went wrong and continues its breathtaking decline. Employees that got jilted in the IPO leave in droves for greener pastures, if they haven’t already. One or more of the recently hired executive team concludes they didn’t sign up for this mess and decides to bail on the company.

Even if they right the ship somehow, it’s hard to have much confidence in a business that is so susceptible to wild swings. The business seems to be more volatile than the stock price right now.

Following earnings, JP Morgan issued a double downgrade and cut their price target to $5. That seems fair to me.

The company still looks to generate ~$1.0 to $1.5B in gross profit for the year, but not even management can tell you what to expect at this point. It’s unclear how much actual cash flow can be extracted from that gross profit, if at all. Including the ~$1.6B in cash remaining, I struggle to justify paying more than $2.5B to $3B for the whole business today. That’s a $4-$5 stock price, and there’s still 70M in options outstanding remaining to be exercised.

The potential upside is uncertain. In this scenario, perhaps these last few months turn out to be a mere blip, a decline artificially enhanced by the COVID highs. Perhaps one or several insiders increases their ownership at these depressed prices. Perhaps the company finds a way to push through as it has so many times before. Maybe the company ultimately resets at a lower revenue baseline with logistics and local, which would still be a $1B revenue business. Or, they just start from scratch with an entirely new app. It’s hard to count out a company with a driven founder CEO at the helm with ~$1.6B to work with (though we’re told not to expect anything until H2’22 at the earliest).

My intent in investing is to buy and hold for the long-term. The hardest part is holding. If I stick my head in the sand and revisit in 3-5 years, this could all potentially play out ok. Stranger things have happened in these markets. As much as I’d like to believe it, which psychological trap would I be succumbing to the most if I counted on that?

The business, as it currently stands, looks broken. What used to be a promising, high-growth, global-scale differentiated commerce player at an excellent value has deteriorated into a meme stock with an unclear future.

I candidly admit that I had quite a bit of conviction in the asymmetric risk reward of this opportunity. That conviction has almost entirely disintegrated. I see as much downside as upside now.

Warren Buffett famously sold all of his airline stock holdings at the COVID low. Based on the information that was known then, I think it was a justifiable decision. Based on the information that I know now about Wish, I think it would be justifiable to exit the position completely, at least until there is evidence that the business has found some stability.

As I said before, it’s hard to count out this company and this CEO. I revisited Joe Lonsdale’s reflections on the Wish investment at the time of IPO in December - seems like such a long time ago now.

In Silicon Valley, many built businesses catering to their wealthy friends – but cost-conscious consumers are a much larger market.

With no one else addressing this segment of the market, Peter realized that Wish could become the e-commerce platform for cost-conscious consumers. Wish could do a better job than the incumbent discount retailers in serving these consumers. Rather than relying on humans to guess what merchandise to stock the shelves with, Wish could predict consumer preferences by gathering data at scale and conducting experiments to figure out which items people actually wanted to buy.

…

Wish’s incredible journey is proof of what happens when you bet on top talent, focus on solving overlooked problems, and persevere.

I do believe those traits are worth betting on. The key missing piece is evidence that there is a viable e-commerce business model to address the cost conscious segment of the market. They’ve had it for years, and lost it for a quarter. Is it too much to think they’ll figure it out and recover? I hope that’s not wishful thinking.

This was a swing and a miss, but I think I still would have swung based on what I knew.

I’m not exiting all the way just yet, but I certainly had way too much exposure based on where the opportunity is today.