Wish is priced like it's going out of business...

Wish is priced like it's going out of business...

But ContextLogic is not acting like a company in decline

Source: Wish apps on Google Play

*** Note: For entertainment and informational purposes only. Not investment advice. Please do your own research. ***

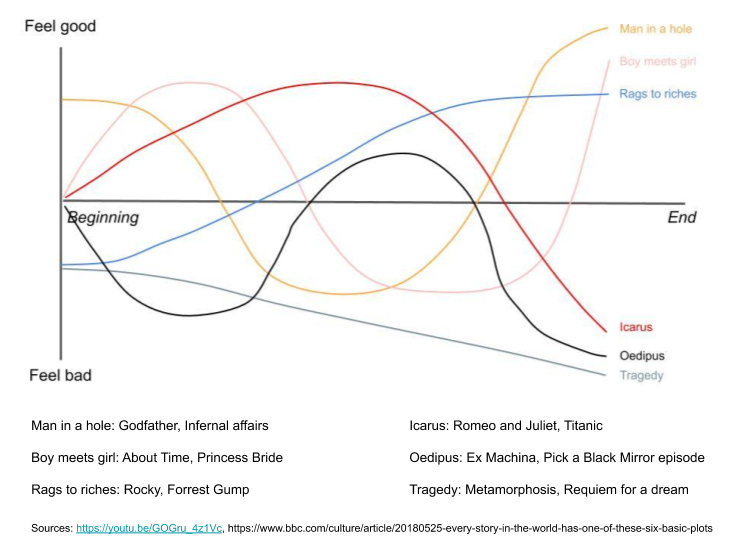

The narrative in the numbers

If stories have shapes, then which narrative shape does Wish fall under?

Source: Avoid Boring People, A Story is a Lie and A Story is True.

At the time of last year’s IPO, it seemed to be the classic Rags to Riches story. A founder CEO, born in Soviet Poland, immigrating to the West, studying math and computer science, working as an engineer at Google and then founding a company dedicated to bringing affordable goods and services to the neglected and overlooked value-conscious consumer globally.

The narrative has shifted. Now it feels like something between an Icarus (rise-and-fall) and a downright Tragedy (fall).

The stock chart certainly maps pretty well. At under $5 per share, Wish is down 80% since the IPO at $24, and down 84% from the all time highs at $31.

Just about everybody is underwater at this point. It’s been a painful ride.

Sentiment has predictably soured. Wall Street is backing away and issuing downgrades across the board.

Source: MarketBeat

What marketplace businesses trade at ~1x gross profit?

At $4.93 and 628M shares outstanding, the current market cap is ~$3.1B. With $1.5B net cash, the enterprise value is $1.6B.

Trailing 12-months revenue is $2.8B and gross profit is $1.6B.

In other words, half the market cap is in cash, and the business trades at ~1x EV/gross profit.

It hasn’t always traded at such low multiples. What has collapsed is the sentiment in the business as reflected by the multiple, and not so much the fundamentals.

Note, there are still 70M options to be exercised and 39M RSUs outstanding. Even with this ~15% dilution overhang, the case that the company is egregiously undervalued still holds in my opinion.

What marketplace business trade at 1x gross profit? Only ones that Mr. Market believes are likely to go out of business.

Reddit reflexivity

I would have thought that Wish entering the Reddit meme stock conversation would have been a net positive. Not only does company’s mission appear to resonate with the Reddit ethos, the actual product mix would have seemed to fit squarely within the customer demographic. At worst, I would have thought it was free marketing for the company.

Now, I’m pretty sure it’s been a negative. Ugly stock performance fuels derisive public sentiment which stains the perception of the product. It’s an unfortunate negative feedback loop. Crappy products sold by a crappy company. No wonder the stock has performed so poorly.

I got caught up in that negative spiral, particularly following a disaster of a Q2.

But then I spent more time revisiting my earlier thesis, reviewing the product experience again, and thinking about where the company might go from here.

For better or for worse, I find myself having more conviction in the prospects of the business than ever before.

How bad is the cash burn really?

For the first half of 2021, the company burned ~$650M in operating cash, taking their cash balance from $2.2B to $1.6B. That looks really bad on the surface.

However, approximately $470M of this negative cash flow impact has been due to reductions in current liabilities (accounts payables, merchants payable, accrued refund liabilities). I’m not sure why they took down their current liabilities so dramatically - from $1.8B to $850M over the past few quarters. Perhaps this is a reversal of their extension of payables at the outset of the pandemic. Perhaps they are unwinding the accounts of low quality sellers. At any rate, the pace of liabilities reduction is unlikely to continue since you can’t cut liabilities past $0.

The actual burn impact from owner’s earnings (net income + D&A) has been closer to ~$200M for H1. It’s still unprofitable, but it’s at least much more palatable than the headline burn figure.

Historically, Wish has carried current liabilities of ~2x revenue, excluding the pop in Q2’20. That ratio has compressed in 2021. I suspect Wish will stabilize or even take current liabilities back up to historical levels relative to revenue, which could potentially have a positive impact on cash flows.

Source: Wish IR

The point is that the cash burn may not actually be as bad as it looks on the surface.

Was Wish just ahead of the curve?

Wish noted that their customer acquisition machine stopped working starting in mid May, and they subsequently cut all ad spend to figure things out. They pointed to the world reopening and Apple’s privacy changes as the primary culprits.

I was perplexed by this development since I had thought Wish’s data science was supposedly their crown jewel.

Since that report in August, many companies have reported absolutely brutal Q3 earnings. For example, Snap fell 25% as its ad business was disrupted by changes to Apple’s privacy terms.

Wish had talked about this effect in their Q2 earnings, noting that even though most of their users are on Android, Apple’s changes caused advertisers to shift their spend to Google and distort customer acquisition costs.

…as more advertisers shifted their spend from iOS to Android, they drove up bids for impressions, limited the quantity of impressions supplied and ultimately increased their advertising costs. These rising digital advertising costs contributed to lower marketing efficiency.

In retrospect, these comments were a harbinger of the incredible blowout earnings that Google reported in Q3.

Cutting marketing spend under such circumstances was the prescient and correct decision, as painful as it was.

There are signs that Wish may be making progress on addressing their marketing efficiency issues. It seems that they restarted paid traffic acquisition starting in September.

Source: Semrush

This is not a complete picture as it does not reflect their mobile app marketing activity, but I’m treating this as a positive indicator nevertheless.

The good news is that management has been in this position before.

In this interview from 2016, Peter talks about how they shut off marketing and ran cash flow positive for 10 months to prove that they could.

From there, they were running the business at cash flow positive leading up to their IPO.

The possibility that the business is in secular decline remains, but I like the odds that this is a temporary blip. We’ll see what they report in their earnings this coming week, but I suspect they may be one of the first ones to come out of this industry-wide setback.

Amateurs talk strategy. Professionals talk logistics.

I spent the past few weeks diving deeper into the user experience, and I came away extremely bullish.

In one case, I made 3 separate purchases - 2 kids hats and a charger - placing orders on Aug. 17 and 19. They arrived in one package on Sep. 3, within the expected delivery date of Sep. 9.

These were inexpensive items and I was satisfied by what I got for the price. I was impressed by the detail of the tracking and how Wish was able to combine the packages at their China facility.

For a separate purchase - a Halloween costume - I tried out the local pickup option at a beauty salon. It worked pretty smoothly, and the proprietor was very familiar with Wish pickups.

I can understand the appeal of the Wish Local program from a business owner’s perspective. It’s free to participate, and you get the benefits of driving customer foot traffic, upselling your own products and services to Wish customers, and earning commissions for every pickup.

There has been a noticeable uptick in locations over the past few months. The below is a map of the Bay Area.

From the buyer side, selecting pickup reduces the cost of shipping. For my order, it shaved the shipping cost from $8 to $4. This will likely become configurable eventually. I could see local businesses wanting to operate small dollar store depots and adjusting the shipping pricing or even offering free shipping to dial up foot traffic.

Delivery times have been reasonable at 2-3 weeks, although the app usually overestimates and guides for 3-4 weeks.

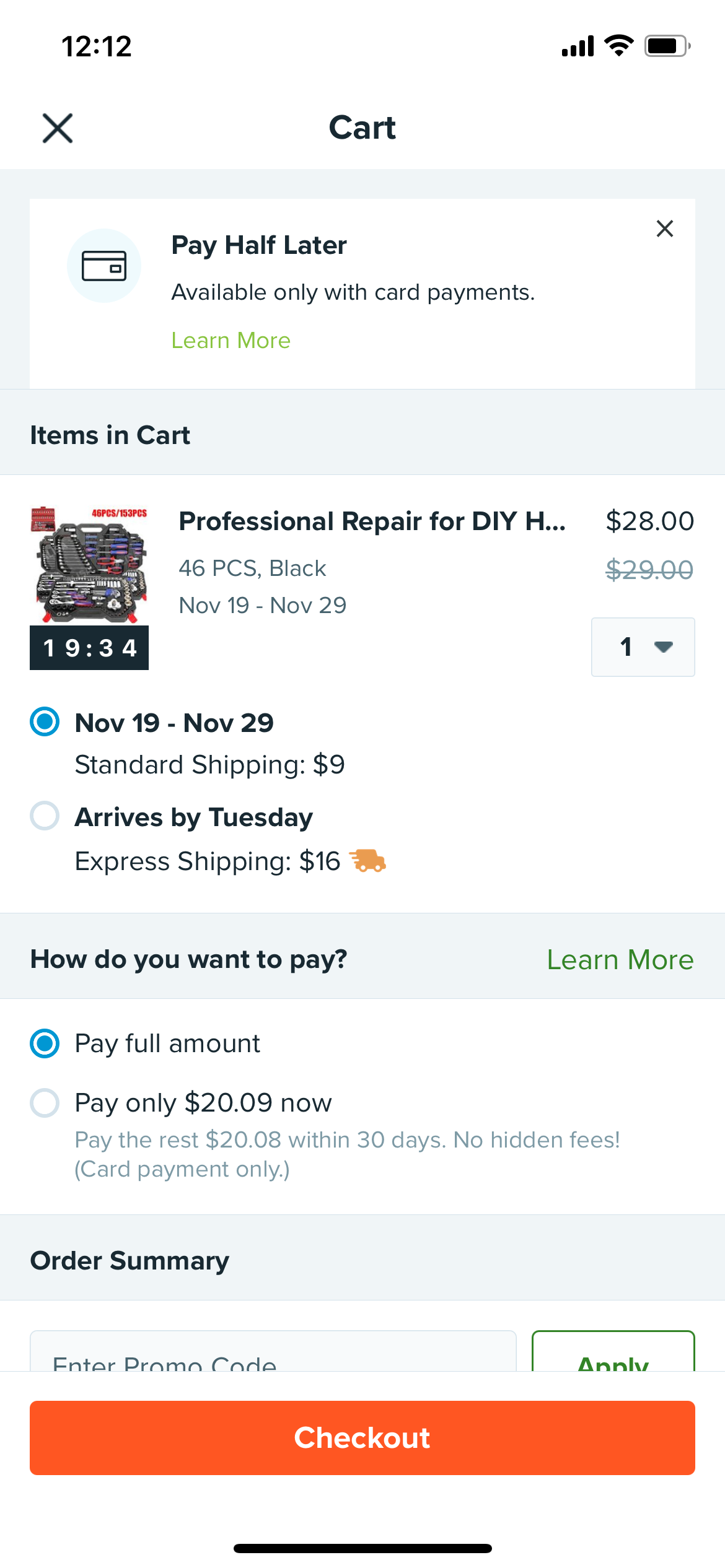

They are also experimenting with buy-now-pay-later options. The below is a capture of what is available today, and they also recently announced an expanded partnership with Klarna.

This is specifically for the U.S. Wish’s fintech opportunities seem tremendous given how much volume around the world they do, so I’d expect a lot more news on this front to come.

Wish has endured a reputation for questionable product quality and lengthy unreliable shipping for practically its entire existence. Perception is hard to change, but that might not be warranted anymore. The logistics and backend, tracing the package from the seller to the buyer, whether direct to the doorstep or via a local pickup option, seem quite solid to me.

Front-end optionality

What the company lacks is a decent front-end customer experience. The current Wish app experience feels cluttered, tacky and irrelevant to me, though I recognize I’m not necessarily their target customer. Though perhaps not, as I do appreciate a decent bargain, and I am guilty of paying down for quality.

However, my hunch is that when you have the backend logistics nailed down, the front end is much more straightforward to swap out.

Frankly, the Wish app and brand may have too much baggage at this point.

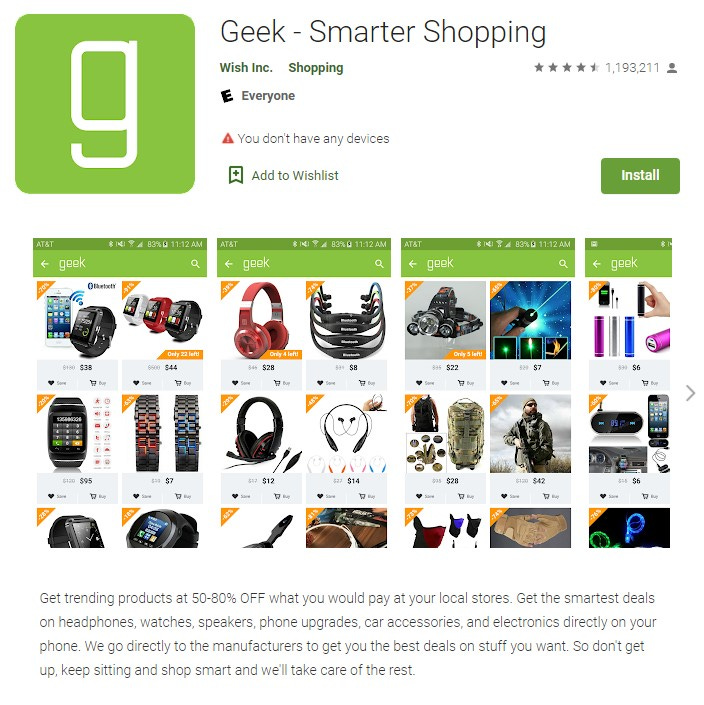

The company has actually been supporting a number of different vertical-focused apps for awhile. For example, they have the Geek app which is tailored to electronics items. It looks like Wish with a different color scheme and different merchandising.

They also have Home for home decor, Cute for fashion, and Mama for maternity and baby items.

1Sansome for social fashion shopping looks like it was only recently released given the low number of installs so far. It is a very different look.

For some reason, the app hardly has any traction (yet).

Turning to Reddit for clues:

Has anyone poked around the 1Sansome (Wish's newest offering) app and compared to Instagram app? They look/feel very streamlined and influencer info identical in many cases.

…

Agreed, it is cool; a properly integrated e-commerce and social media platform is sort of the holy grail of targeted marketing and creating a "fun" shopping experience. Thus far i don't think Facebook marketplace and Instagram shopping have done a great job executing. Perhaps with Wish's infrastructure and rapidly evolving global logistics (e.g. Wish local, Wish wholesale, the other targeted apps - 1S, Geek, Mama, Home etc...) such a partnership would make for a formidable global e-commerce play at truly competing with AMZN and BABA 🤔 Add in a fintech component and we are talking new world order.

Also agree, 1S having so few followers is weird... Frankly, the entire roll out of 1S is weird. It's been done very quietly; not even a press release on Wish's IR website. Even the popular influences with 250k+ followers on Insta, only have a handful of followers on 1S and the #wishfluencer tag is not used frequently anymore. It all kind of feels like a decently polished Beta environment... but why? The only thing I can think is that there is something very big in the works, and it is a self imposed quite period during testing OR there is some serious execution/communication failure on the company's part. Given the number of job posting on LinkedIn (188 at present), and other tea leaves, the former seems more likely.

The best answer is given by the questioner.

1Sansome is a ContextLogic trademark. 1Sansome on the Wish app looks like any other generic private label fashion brand. It may be that this is just one of many company experiments that doesn’t go anywhere. Or, it may be the beginning of a vertically integrated response to Shein (estimated private valuation of $30B), with more social and video elements and access to a broader local pickup network.

However this turns out, I like the experimentation.

The advantage of having a controlling founder CEO at the helm is that these calculated pivotal long-term bets can be made.

People

It is encouraging that there are now other seasoned executives to help carry out the vision.

This was the management team a year ago at the time of IPO. They effectively only had three C-level officers then.

This is their management team now.

They’ve added Jackie Reses at Exec Chair (May), Farhang Kassaei at CTO (July), Tarun Jain at CPO (August), and Vivian Liu at CFO (October), all of whom come with impressive backgrounds. They are probably still missing a CMO, COO and CRO, but it’s a much fuller and improved executive team now.

I was admittedly worried about the risk that some of these recent hires might quit after last quarter’s debacle. With years of tech experience under their belts from the likes of Square and Google, none of them needs to work. They could easily choose to back out if they didn’t want to be there. That <knock on wood> hasn’t been the case.

The only person to have checked out is Ari Emanuel, who resigned from the Board in September. That might be ok as he has a lot on his plate with Endeavor. Interestingly, Reses joined the Endeavor board in August.

I’m not quite sure what to make of Reses’ day-to-day role or how involved she actually is in the business. In her bio, she seems to define herself first as the CEO of Post House Capital position. Maybe her value is more to signal the company’s fintech aspirations rather than the actual operational blocking and tackling. As a well-connected billionaire, someone who introduced Bill Ackman to UMG as part of Pershing Square Tontine, why exactly is she choosing to spend so much time on a piddling $3B market cap e-commerce company anyway?

I suspect there is more value here than the market is giving them credit for.

Hopefully one or more of the new execs will join Peter on future earnings calls. It sounded kind of lonely up there during the Q2 call.

The company also continues to hire.

There are now 1,100 employees, up from 828 at IPO. There are close to 300 jobs on their careers page, with interesting indications of where the company is headed: video, payments, incentives/games, merchant ads platform, logistics as a service.

If the company is really on the decline and going out of business, they certainly do not seem to be acting that way.

Mr. Market throws a knuckleball

It’s been humbling and lonely to be a Wish bull lately.

This company has a ~$3B market cap, trades at 1x gross profit and 2x their $1.5B cash balance.

This was a company that grew revenue from $144M in 2015 to $2.5B in 2020 and did it at roughly breakeven.

I think the current price makes sense if the company were to collapse over the next 5 years as quickly as it grew in the prior 5 years. It’s not being run this way, but if it really came to it, I believe you could cut marketing and extract $1.5B+ in cash flows before the ice cube melted.

The market seems to be bracing for a dismal showing in Q3, a continuation of the 30-40% declines experienced in portions of the business in Q2.

If the company does anything better than that, then it seems the business is severely undervalued.

In fact, I really like the company’s prospects, and I suspect the seeds being planted will eventually yield tremendous fruit. The market is valuing the business like it’s going down the drain, while I think the company is just getting started.

I continue to think a stock buyback announcement (i.e., the board just authorizes a buyback) makes sense.

I would love to see some insider purchases if the stock price remains at these levels following earnings.

In baseball, knuckleballers typically befuddle hitters who can’t deal with their fluttering unpredictable pitches. Every once in awhile though, the knuckler throws a flat pitch, which typically ends up in the stands.

The current setup in Wish is about as fat a pitch as I’ve ever seen. The market is telling me that I’m an idiot though. Perhaps I am. But you can’t hit home runs if you’re afraid to strike out.

Which narrative shape does Wish fall under? I believe we’re watching a Cinderella story. I’m willing to wait to watch it unfold.

*** Note: For entertainment and informational purposes only. Not investment advice. Please do your own research. ***